TL;DR: There are increasing signs in economists’ forecasts, auction clearance rates, migration rates, divergent tax policies and house building rates that a clear victory for National/ACT in the October 14 election could unleash an immediate 10-20% bounce in house prices in auctions and open homes in late October and November.

A similar thing happened in the wake of the mid-September 2014 election, when investors celebrated the death of Labour’s Capital Gains Tax proposal after then-National leader John Key trounced then-Labour Leader David Cunliffe in debates over Labour’s CGT plan. See more below the fold.

News elsewhere from Aotearoa’s political economy on climate, housing and poverty:

ANZ’s economists have picked a bottom in the housing market and forecast prices would bounce around 8% over the next 18 months because strong net migration was outpacing new house-building;

Stats NZ has reported dwelling consents have fallen by at least a quarter in the last four months and house-building is now at least 3,500 dwellings slower than it needed to be go cope with net migration of 43,000 so far in 2023;

The He Waka Noa talks to limit farming emissions appear to have finally collapsed behind the scenes, meaning officials are now actively looking at imposing a fertiliser tax speculated at $150 per tonne or $91 million per year; Politik-$$$

Housing Minister Megan Woods has tried to resurrect the bi-partisan housing densification accord with National, but Christopher Luxon appeared to rule out any compromise on his new MDRS-lite approach favouring greenfields’ developments over inner suburban townhouses; RNZ

But bipartisanship might not be dead yet on transport, with BusinessDesk-$$$’s Oliver Lewis reporting this morning from an interview with Michael Wood that a bipartisan deal on congestion charging was possible before the election;

Hundreds of residents from yellow and red-stickered homes flooded in the Hale and Gabrielle cyclones are bracing for Government and council decisions to be published tomorrow tomorrow on the prospect of managed retreat and compensation; Stuff

Auckland Mayor Wayne Brown is set to present his final Budget proposal later today, but he appears to be back-tracking on an earlier back-track at the last minute. In an interview with Bernard Orsman published this morning in The NZ Herald-$$$, Brown threatened to reverse his previous softening of cuts to arts and social services spending unless Labour-aligned councillors Richard Hills and Shane Henderson switched back to their original plans to sell Auckland Airport shares to stop the cuts Stuff; and

Overseas, Russia threatened retaliation at Ukraine after drones launched from outside Moscow exploded and fell on residential areas in Moscow and more than 350 AI executives, researchers and engineers published a joint one-sentence statement:

"Mitigating the risk of extinction from AI should be a global priority alongside other societal-scale risks such as pandemics and nuclear war." 350 AI experts in a joint statement.

Usually, I put in a paywall for paying subscribers at this point in the email newsletter and lock off the podcast above from free subscribers. But I want to experiment until the end of June with publishing everything to everyone immediately to see what happens with subscription rates, revenues and email opening rates. I want to thank paying subscribers in advance, who are still the only ones able to comment and get access to our very active chat section and webinars. Join our community by subscribing in full to support my journalism in the public interest about housing (un)affordability, climate change (in)action and poverty (not enough) reduction.

House prices primed to surge 10-20% if National wins

It’s like deja-vu all over again.

House prices are primed to surge 10-20% soon after any clear National-ACT win on October 14 because:

house building is again rapidly falling behind population growth from migration;

investors are salivating over the potential for valuation-boosting return of interest as a taxable expense; and,

a change of government is expected to both lower borrowing costs and widen a housing supply deficit.

The last time Aotearoa faced an uncertain election result and the potential for a real estate tax change was in 2014. Cunliffe’s fumbling of a Key challenge about the CGT effectively being an inheritance tax on family owned assets in a debate in Christchurch was the spark. House prices rose 10.3% in the nine months after National claimed a third term in September 2014 and by a full 37% during the 2014-2017 third term, although they also went on to rise a further 143% between the election of Labour in late 2017 and now.

A clear win would be the spark into a very dry pile

This time on the eve of a ‘third term’ election, there is even more dry kindling on the housing market pile to catch fire if National/ACT win clearly in their own right, including:

National/ACT’s promise to repeal Labour’s interest deductibility rules, which would significantly improve the investment case and borrowing capacity of rental property investors1;

National/ACT’s promise to wind the ‘bright line’ test for taxing income from capital gains from landlords back from 10 years under Labour to National’s original two years;

A likely further immediate slowdown in new house building and consenting if, as expected, National freezes new infrastructure and Kāinga Ora investment to reduce Government spending;

A faster reduction in the Budget deficit and Government borrowing, which would drag down mortgages rates faster than under Labour, all other things being equal; and,

An expected further loosening of migration settings to bring in more lower-paid workers to fill labour shortages, which would further increase demand for rental property and reduce wage and interest rate pressure.

All the signs the market is about to bounce are there

Even before the result of the election is know, it’s clear the momentum in the housing market is shifting, with a range of forecasters revising their house price forecasts up in recent weeks.

Te Pūtea Matua (The Reserve Bank) revised its forecasts last week for house prices by 7.8% from its February forecasts, pointing to the rise in demand from migration, both of temporary workers and big surge in those getting residency visas that allow them to buy property.

Between September 2021 and July 2022 the Government made it temporarily possible for immigrants on work visas who met certain criteria to apply for a special resident class visa.2 More than 93,000 applications have been approved so far, increasing the pool of people eligible to buy residential property in New Zealand.

This factor, when combined with strong net immigration, has led to a less negative outlook for house prices. While the outlook for house prices is highly uncertain, house prices are assumed to fall by less over coming quarters than assumed in the February Statement. RBNZ in May MPS (Page 14)

Without any change of Government, Reserve Bank forecast house prices would begin rising in absolute annualised terms by the end of next year. The peak to trough decline from 2021 to 2023 would be closer to 17% than the previously forecast 23% fall.

The Reserve Bank’s decision to keep its forecast peak in the Official Cash Rate at 5.50% also removed any immediate prospect of any further rises in fixed mortgage rates, helping to bolster house value prospects.

Actually, average fixed mortgage rates for two year and three year terms have fallen by 10 basis points and 40 basis points respectively since December. The two-year and three-year wholesale ‘swaps’ rates that the fixed rates are based on have fallen by 30 basis points and 20 basis points respectively since December, Interest.co.nz data shows. Wholesale interest rates are now only just above where they were during the 2014 election campaign and three-year fixed mortgage rates (6.23%) are actually slightly below where they were in the 2014 election campaign (6.45%).

National/ACT have yet to detail their fiscal policies and how much further downward pressure they would put on interest rates, but National Leader Christopher Luxon and ACT Leader David Seymour have both emphasised they would be tighter with the ‘purse strings’ than Labour. They have also promised tax cuts of some kind, which would increase disposable incomes for home owners already flush with equity to further leverage up their investments with more purchases.

There is ample potential for lower interest rates, more borrowing, less housing supply and more population growth to increase prices by another 10% on top of the tax change benefit of 10%.

Green shoots are popping up all over the place

Swapping metaphors, a change of Government would add water and heat to a market already showing plenty of green shoots, as ANZ’s economists pointed out yesterday in their monthly property market note titled: On the floor, ready to floor it?

ANZ increased its own forecasts by around eight percent, even with another rate hike that the Reserve Bank is not itself expecting.

Here’s ANZ’s reasoning (bolding mine):

“The RBNZ’s relatively muted response to surging netmigration and additional fiscal stimulus in the May MPS surprised us. Ultimately, for a time at least, this implies looser monetary conditions than we have been expecting. This, combined with surging net migration and the confirmed loosening in LVR restrictions from 1 June, has led us to upgrade our house price forecast. '

“We now expect quarterly house price inflation to return to around its historical average pace over the second half of 2023 before sticky inflation (and its implications for the OCR outlook) puts renewed upwards pressure on mortgage rates. Net migration is a huge wild card for the outlook currently.

“The recent explosive pace alongside slowing construction activity is resulting in a rapidly widening housing deficit, adding pressure to house prices. In short, housing tailwinds now appear to be blowing a little stronger than the headwinds.” ANZ economists in their May Property Focus note.

In particular, they focused on the growing supply imbalance as housing supply growth stalls and population growth from net migration surges.

They also noted tight supplies of houses for sale as owners who are not any pressure from their banks wait for the election, rather than take low prices now.

“While sales are low, new listings are also very weak, and that’s helping to keep the market relatively tight. Low levels of new listings also suggest that households and investors aren’t being forced (at least en masse) to sell up because of rate rises.

“Putting it all together, we are seeing a tentative tightening in the market, with the number of properties available for sale off recent highs.

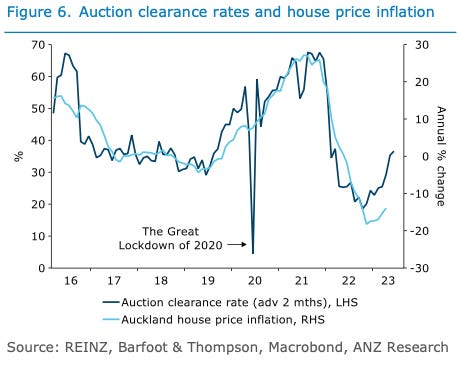

“Auction clearance rates in Auckland certainly suggest this market is coming back to life quickly, and even suggests some upside risk to our forecast.” ANZ economists.

ANZ’s economists also pointed for the potential for changing LVR rules and tax settings to turbo-charge the rebound.

“Policy changes will matter too. The LVR changes could provide a near-term shot in the arm, but even more important is the future of the deductibility of interest payments on investment properties when calculating expenses for tax purposes.

“It’s uncertain whether the risk in practice is that the non- deductibility policy staying will cause a flurry of sales, or whether the policy going will cause a rush of purchases. But either way it’s potentially a big driver of the market this year.” ANZ’s economists

The potential for the election result to be an inflection point for house prices is strengthening, further raising the stakes in the election campaign for land owners and renters.

Just as our economy is a housing market with bits tacked on, our political calculus is often also a housing market with bits (taxes, migration settings, fiscal policy, state house building) tacked on.

Ka kite ano

Bernard

Westpac’s economists estimated in this March 2021 note that the imposition of the policy could reduce house prices by around 10%, although the full removal of deductibility does not kick in until April 1, 2025 and the phasing in the removal of interest as a tax deductible expense currently stands at 50%.

Share this post