Long story short: Reserve Bank Governor Adrian Orr has resigned unexpectedly and without explanation, three years before the end of his second five-year term. Finance Minister Nicola Willis and soon-to-be Deputy PM David Seymour never wanted the-then Labour Government to reappoint him in late 2022, arguing (with hindsight) his actions worsened the 2022-23 inflation shock by stimulating the economy too much and criticising his increased regulation of banks for stifling competition.

The big four banks also opposed Orr’s pre-Covid drive to make them hold much more of their own capital to back their loans, and to restrict highly-leveraged lending to rental property investors. Without having to change interest rate policy, a replacement could loosen those rules to try to fire up more competition in banking, which risks creating a new 2004-style ‘unbeatable’ mortgage war and another credit-fuelled housing price boom.

Done fast enough, that wealth effect and surging house sales volumes would in turn unlock much stronger consumer and construction spending in an economy which remains a housing-market-with-bits-tacked-on because of a lack of affordable new housing supply. Such a splurge credit-fuelled economic growth might be big enough and fast enough to get the Government’s political support ‘back on track’ ahead of the 2026 election.

It will depend on who Willis appoints, how quickly she does it, and whether the central bank loosens those bank capital and rules for lending to landlords fast enough to trigger a pre-election boom. The clock is now ticking, for both the housing-market-with-bits-tacked-on, and the Government.

(I spoke with CTU Economist

in a live video chat for paying subscribers last night. It is published above for all to watch now. Usually, there is more detail, analysis and links to documents below the paywall fold and in the video or podcast above for paying subscribers, but I’m opening this up immediately for full public watching and reading, given the public interest involoved.Usually, If we get over 100 likes from paying subscribers we open it up for public reading, listening and sharing, although we’d love it if you subscribed to support our ability to make this journalism public. Remember, all students and teachers who sign up for the free version with their .ac.nz and .school.nz email accounts are automatically upgraded to the paid version for free. Also, here’s a couple of special offers: $3/month or $30/year for under 30s & $6.50/month or $65/year for over 65s who rent.)

Unpopular with the Govt & the big banks, Adrian Orr resigns

Adrian Orr appeared to surprise everyone early yesterday afternoon by announcing his immediate resignation as Reserve Bank Governor, just two years into his second five year term. The (still) unexplained reason for the departure has added to the mystery and shock, although the financial market reaction was much more muted.

In any other country where a decidedly independent central bank governor who was often at odds with his finance minister resigned without reason, there would have been market chaos. Perhaps the institutional and constitutional buffers between and around the bank and Government were enough to reassure traders and investors, or perhaps the current weakness of the US dollar in the wake of Donald Trump’s latest tariff shocks was enough to calm the farm.

Orr didn’t include a reason for his resignation in his statement, Willis said1 she wouldn’t say, and left it to RBNZ Chairman Neil Quigley to give more detail in a hastily arranged and unusual 5pm news conference. Quigley, in turn, was also frustratingly non-specific about the reason/s, other than to say2 Orr felt ‘it was time.’

Quigley did suggest there had been tension between the bank and the Government in recent weeks over its 2025 Budget round funding proposal, which others3 have reported was for an increase at odds with the Government’s expectations. But the chairman didn’t confirm suggestions that either the latest funding debates were the trigger or some sort of straw that broke the camel’s back, or there had been some sort of performance or behaviour dispute.

Whatever the case, Orr is now gone and using up his leave before the formal end of his employment. His deputy, Christian Hawkesby, is now the acting Governor until March 31, from when the Government will have up to nine months to appoint a permanent replacement for the next five years.

So what now? First, some context and background.

The public became aware of the current Government’s antipathy to Orr in late 2022 when then-Opposition Finance Spokeswoman Nicola Willis wrote a letter to then-Finance Minister Grant Robertson to protest at the reappointment of Orr to a second five year term without consulting with the Opposition in the leadup to the 2023 election. ACT Leader David Seymour had been even more critical of Orr’s operation of monetary policy and bank regulation.

But unhappiness had been swirling around the banking system well before the Reserve Bank’s actions during covid. Orr led a dramatic increase in capital requirements for the banks from 2018 to 2020, arguing they should have enough to cope with a 1-in-200 year financial crisis, rather than the global standard of 1-in-100 years. The banks pushed back hard, saying it would force them to hold more of their own expensive capital in reserve in a way that increased costs for customers, and would make it harder for new entrants to compete.

The banks were also less-than enthused about the central bank’s proposals, now enacted from July 1 last year, for limits on debt-to-income multiples (DTIs). They were designed to act as a guardrail to limit future lending to rental property investors as interest rates fell. Mortgage brokers now report the DTI limits are kicking in and frustrating rental property investors wanting to buy more properties.

The economy’s very slow recovery from its per-capita recession through 2023 and 2024 under the weight of high mortgage rates is becoming equally frustrating for the Government. What it needs now is the usual surge of mortgage lending to fire up the economy through the wealth effect and cash surges from a jump in house sales volumes and prices, but the DTIs are frustrating that, as is a lack of competitive tension between the banks.

‘Show us the competition’

Willis also wants more competition in banking to force banks to pass on more of the benefits of lower interest rates to mortgage borrowers and businesses. She and others have argued the Reserve Bank’s increased regulatory and capital requirement zeal has thrown a blanket over those competitive urges.

A replacement for Orr who loosens the capital requirements and lowers the DTI limits would create the conditions for another 2003-to-2007-style mortgage lending boom, fueled by the BNZ’s ‘Unbeatable’ campaign to ‘beat’ any competitor’s two-year fixed mortgage rate. There was also a fresh surge of competition through 2011 and 2012 as ANZ under then-CEO David Hisco fought to increase ANZ’s market share in Auckland as it ramped up for the merger of its ANZ and National brands.

It was only the introduction of Loan to Value Ratio (LVR) controls in 2013 by then-Governor Graeme Wheeler that put a dampener on the housing market again, before ever-lower interest rates in the lead-up to covid helped accelerate things again. Orr’s Covid-era decisions to print money to lower longer-term interest rates, to lend very cheaply to banks so they could in turn lend cheaply to home buyers, and to remove the LVR controls in 2020 that lit the blue touch paper on the housing market and the economy through late 2020 and 2021.

The blue touch paper is ready again. It just needs a new Governor with the ‘right’ approach to getting our housing-market-with-bits-tacked-on economy ‘back on track.’

The only question is how fast the match can be struck.

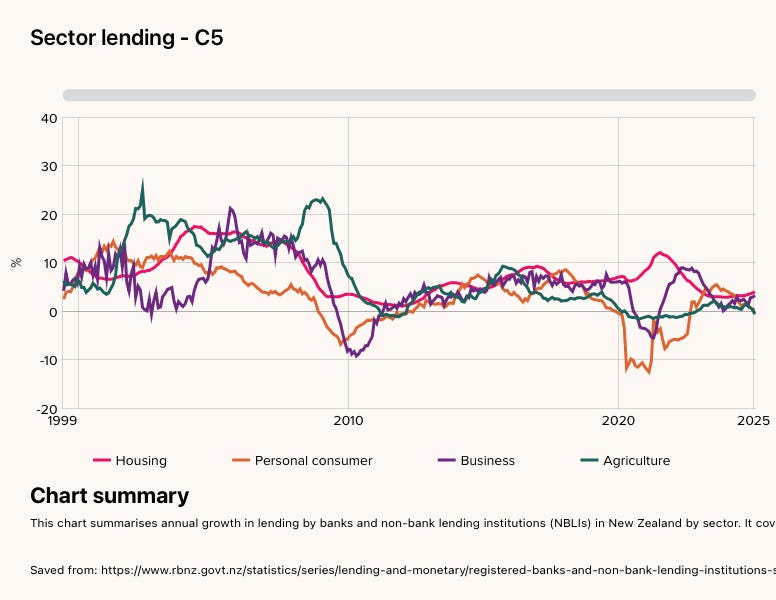

What the previous booms looked like (follow the red line)

Thank you

, , and many others for tuning into my live video with ! Join me for my next live video in the app.Ka kite ano

Bernard

Analysis by NZ Herald-$$$’s Thomas Coughlan last night.

Share this post