TLDL & TLDR: The Reserve Bank went out of its way yesterday, as it held the OCR at 0.25%, to warn buyers that the housing market ‘appears to be above its sustainable level,’ but it did not go as far as forecasting a massive return to reality.

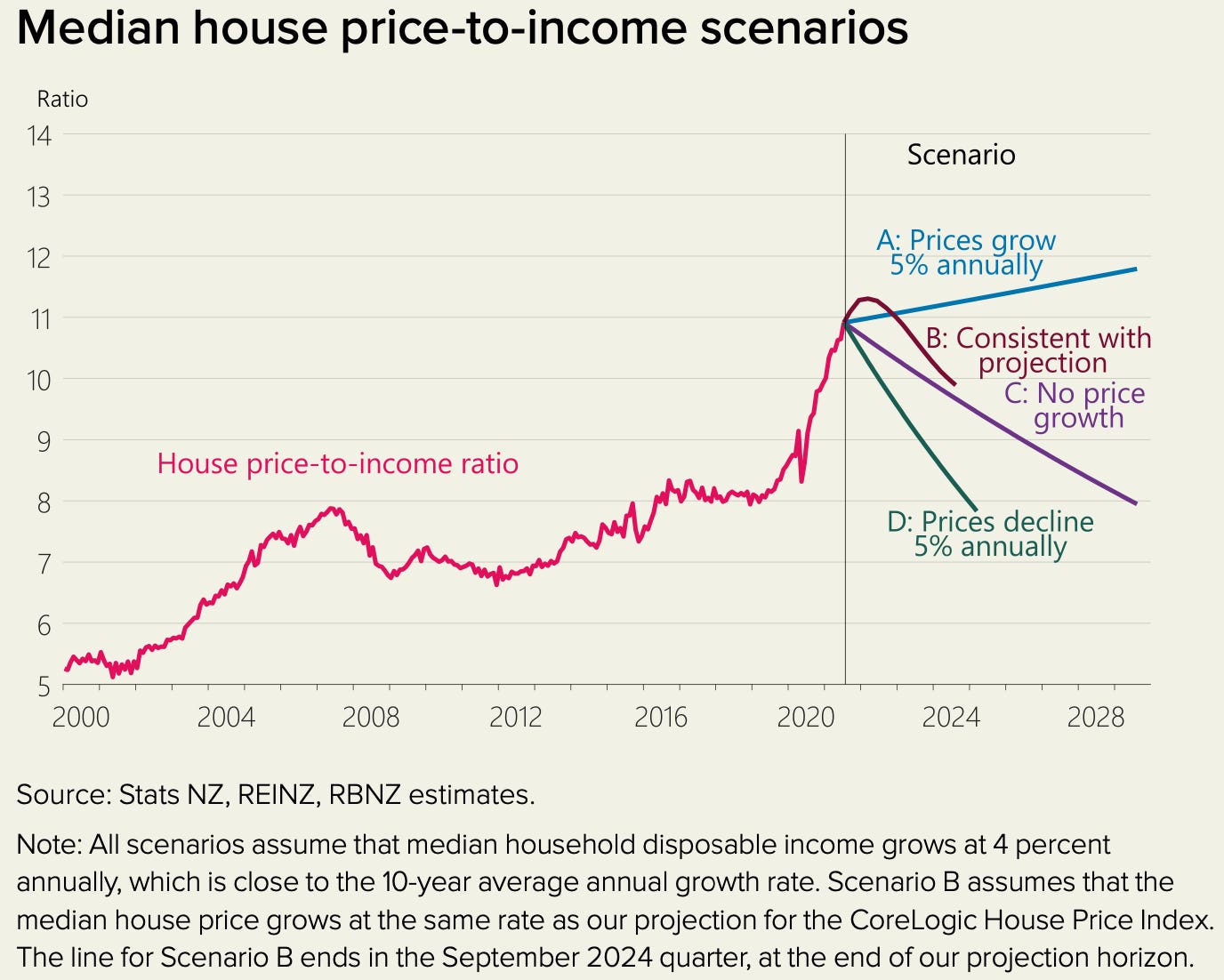

It actually sees house prices 5% higher in three years than it does now, albeit falling towards the end of that period.

The Reserve Bank forecast in its August Monetary Policy Statement the CoreLogic House Price Index would rise another 10% over the next year, before falling back gently by a total of 5% by September 2024 (line B above). Its forecast stops then. However, it did include in Box A (page 17), a detailed discussion of why it saw the market as potentially above its sustainable level and how long it might take to return to something more sustainable, although it didn’t say where it thought sustainable actually was. It also included a projection where house prices fell 5% annually for three years (line D above). Just to keep us all awake, and some fun, for some.

In which I ask Adrian Orr some questions

I asked Governor Adrian Orr about how much prices could fall and where exactly the sustainable level of house prices might be as a multiple of income. I’ve included the exchange in the podcast above. He was careful not to be specific about where sustainable was, detailed all the reasons why prices could fall in real terms. I’ve included the full response for completeness. The bolding is mine.

“We talk about the level of house prices currently compared to what we think would be a more sustainable level. By sustainable we're talking about what we can explain where house prices would be given demand population, and people put houses and supply the number of houses that are available. And we are very adamant in here that current house prices are above what we would call that sustainable level.

“I can't go as far as to say exactly how much because, sadly, I'll give you the glib answer of ‘that depends.’ But I can give you plenty of indicators of why we think they are above sustainable. The first one, of course, is the increase in housing supply that is coming onto the market effectively from end of this year onwards. I think we're seeing the largest increase in housing supply since the early 1960s. And that is coming at a time when New Zealand's population growth is at one of its lowest growth rates. So supply is going to outstrip marginal demand. And that would naturally have a downward impact on house prices.

“Current house prices should be reflecting the current pressure. More supply means further downward pressure on that house price. The other types of measures that we look at are really around long term debt to income ratios, housing debt, mortgage debt relative to household income is at a very stretched levels. And that means that any small increase in interest rates has a magnified impact on debt servicing and debt servicing across households is also at a stretched level.

“So it means the new buyer, the marginal investor in a house is taking on a significant level of debt and interest rates that may be going up. And so again, not only just demand and supply, but the price of debt. And the debt servicing component means downward pressure on house prices, less ability to leverage into homes. And as you're aware, there have been many other policies on housing recently, which all have a dampening effect on house prices -- the tax changes discussed by government and our loan to value ratios, as well as the ones that we are consulting on, and debt servicing ratios. So from our view, the current house prices are above sustainable levels.” Adrian Orr

I then asked him where the sustainable house price to income multiple might be. He responded with the following (again the bolding is mine):

“The first thing is I can talk around sustainable house prices, I can look at actual house prices. And we can talk about corrections. What I can't do is tell you when or by how much, because these are asset prices — they're highly volatile, and they’re captured by the spirit of people buying these assets.

“So I'm talking around the blank, unemotional economic events. What we see through time is house prices can fall, do fall, usually in real terms, once adjusted for inflation. But when we're at low inflation, they can fall in nominal terms. And we have a projection where house prices — we previously had them finishing at zero — we've now got them going slightly negative. I think it's around a minus 5%.” Adrian Orr

Negative OCR more likely than more QE?

Another interesting feature of the MPS and the discussion afterwards was a strong reiteration of the Reserve Bank’s view that it’s preferred tool for monetary policy was the Official Cash Rate (OCR). Most assumed that meant any tightening would be done through rate hikes rather than buying back Government bonds, but I asked whether it meant any loosening required, if the delta outbreak required extended lockdowns, would be done by cutting the OCR to negative levels and allowing banks to use the Funding for Lending Programme (FLP) to ensure the negative OCR flowed through to the economy, rather than restarting the money printing and bond buying programme.

My view: One advantage of negative rates and using FLP is the banks (so far) have prioritised using the cheap FLP money to lend for new house builds, rather than pumping up the prices of existing houses. Expanding that new house build lending would be useful.

Here’s Orr’s response (again bolding is mine.)

I'm pleased you have reminded people that banks are capable of having the negative interest rate. So again, that's a hypothetical answer with a conditional. It's incredibly hypothetical.

What we're talking about in our document is the country being able to manage periods of disruption created by these virus outbreaks. We are in a much better position to manage it via fiscal policy.

We understand what those policies are and how they can be used effectively. Monetary policy will be there to support. Our biggest concerns at present are not about lowering the OCR. It is about making sure inflation expectations are well anchored. So I don't want this conference to get confused. I want this conference to understand that our general path is to be tightening monetary conditions, not to be worrying about negative interest rates.” Adrian Orr

Can we get too far ahead of the pack?

I then asked if he was worried New Zealand might be getting too far ahead of other central banks in other developed countries. NZ would have been the first to hike and most aren’t expected to hike until well into next year. He said we were different. The bolding is mine.

“It's just a base fact that we run monetary policy for Aotearoa-New Zealand, not for not for these other countries, New Zealand has been less impacted to date from the COVID-19. That means our economy has been stronger, we've come up against capacity pressures sooner, and hence, monetary conditions may need to move sooner.

And so it's a very strong and positive position to be in. That's well recognized. We've done a lot of searching across countries to assess for differences. And most of the differences come down to starting point and strength, than anything else. Likewise, it goes for asset prices and house prices.

We've seen asset prices rise globally, again, in part due to the lower interest rates, but the magnitude and timing of that has really been as much related to supply constraints differences across countries. So similar experiences, probably T-plus six months, ahead of some countries. There was a queue of countries talking about what we are talking about today, so we aren't actually on our own. And most of those are small open economies like New Zealand.” Adrian Orr

Scoops and news breaking here this morning

This won’t be easy or quick - There are now 10 cases in the delta cluster and more than 60 locations of interest, including the Central Auckland Church of Christ, where 230 people from all over Auckland attended a service on Sunday with an infectious parishioner. (Newshub) (RNZ)

I’m in the wrong job - Kate MacNamara reports from OIA documents via NZ Herald-$$$ that MBIE spent $133,600 on PR services when organising to buy vaccines. That’s on top of the 64 PR people they have on staff.

In the global political economy overnight

‘Send them to us first’ - The US says it plans to offer booster vaccine shots from September 20 after an Israeli study released this week showed evidence of waning immunity from COVID-19 vaccines in the months after inoculation. (Reuters) Although the WHO says the most vulnerable people worldwide should be fully vaccinated before high-income countries deploy a top-up. (Reuters)

Ready for this? Bankers all over the world and a few consumers should know Facebook announced its ‘Novi’ digital wallet was ready to come to market. (Nasdaq)

Signs o’ the times news

‘I’ll show you unsustainable’ - As the Reserve Bank said house prices were unsustainable yesterday afternoon, an online auction saw a renovated five-bedroom bungalow on Kenny Road, in Remuera (outside of double grammar zone) sell for $5.2m after 5 bidders drove the price to $400k over the reserve & $1.8m above 2017 CV.' (One Roof)

MIQ pain intense - Here’s another example of the grief surrounding shortages of MIQ places. There is a political vulnerability here, given the Government has arranged its own allocation of places that it uses for various things, including the PM said yesterday, bringing back 37 translators from Afghanistan. In this case a pregnant woman wanting to come home to have her child has been refused six times. (Newshub)

The horse has well and truly bolted - New South Wales reported 633 new cases and three deaths yesterday. Now an epidemiologist advising the Australian Government, James McCaw, says cases will likely continue to rise in the next month into the thousands per day. (SMH)

Useful longer reads

Some fun things

Ka Kite ano

Bernard

Share this post