TLDR: We’re discovering all over again how hard it is to go cold turkey on our economy’s addictions to imported low-wage labour and leveraged-and-tax-free gains on residential land price appreciation.

This week’s backsliding by the Government on its hopes to wean NZ Inc off cheap migrant labour shows that, along with the continued ruling-out of wealth or capital gains taxes by Prime Minister Jacinda Ardern and PM-in-waiting Christopher Luxon ‘in their political lifetimes’.

The older home-owning median voters in the suburbs of our big cities and provincial towns and cities cannot imagine a different way of doing things. More importantly, they cannot see how going turkey would be anything other than disastrous for their own plans for retirement and their hopes of helping their own children into stable homes ie the ladder to financial security.

Ironically, but perhaps not surprisingly, the more extreme the addiction has become and the more obvious it is it needs kicking, the harder it is to kick. Median voters and the politicians that court them cannot see an alternative.

There is no alternative (to a residential land tax)

Without too much fanfare, the Labour Government has just reversed its course on one of its main economic strategies. It had hoped to use Covid as a chance to re-set NZ Inc’s addiction to low-wage temporary migration, which has been a key ingredient keeping our economy growing faster overall than our peers for most of the last two decades.

The record-high migration has also disguised the highest rate of ‘leaching’ of home-grown talent in the developed world and even-more-slugglish productivity growth than the rest of the world. It also fueled an explosion in house values to the highest in the world, relative to incomes and rents, that made it palatable for those with homes to still be on low incomes. Low wage migration goes hand-in-hand with leveraged and tax-free capital gains on residential property to keep NZ Inc feeling wealthier than it actually is – for asset owners.

Here’s what was written in a Cabinet paper late last year as the then-Immigration Minister Kris Faafoi was finalising the Government’s ‘rebalance’ of migration policies

“The Rebalance aims to support a future economy that is less reliant on lower-paid temporary workers, better addresses productivity, skills, and infrastructure challenges, and increases the skill levels of migrants. As part of work on the Rebalance and ‘Reconnecting New Zealanders’ step three border opening, interim settings are being developed that would bridge the gap between current tight border restrictions and future settings, while managing and phasing the skill mix of workers entering the country. These include enabling entry of temporary migrants who earn 1.5 times the median wage without other tests.” MBIE advice in Cabinet paper

A quick reminder of the problem

Here’s how Faafoi’s office expressed the problem in a strategy paper to Cabinet last year (the bolding is mine):

“Immigration is important to New Zealand but the volume and mix prior to COVID-19 was starting to impact on our economic performance and standard of living.

“There is no question that New Zealand is always going to need migrants. Migrants make a valuable and significant contribution to New Zealand, both economic and social. And immigration is an important factor for meeting this Government’s goals of creating jobs, supporting small business growth and enhancing our global position. We need to ensure that migrants who are choosing New Zealand as their home have good opportunities, and are not subject to exploitation or poor quality jobs.

“However, our pre-COVID reliance on temporary overseas workers and rate of population growth have been recognised for placing unsustainable pressure on our infrastructure (such as housing and transport) and placing downward pressure on New Zealand workers’ training, wages, terms and conditions.

“A rebalance would aim to improve outcomes for New Zealanders and enhance our economy. This approach is predicated on the basis that businesses previously reliant on migrant workers to fill low-skilled or low-paid roles would be incentivised to find other ways to address their labour needs, such as improving wages or conditions, recruiting or training New Zealanders, or increasing automation.

“The Rebalance aims to support a future economy that is less reliant on lower-paid temporary workers, better addresses productivity, skills, and infrastructure challenges, and increases the skill levels of migrants.

“As part of work on the Rebalance and Reconnecting New Zealanders step three border opening, interim settings are being developed that would bridge the gap between current tight border restrictions and future settings, while managing and phasing the skill mix of workers entering the country. These include enabling entry of temporary migrants who earn 1.5 times the median wage without other tests.” Kris Faafoi’s office in a strategy briefing paper to Cabinet.

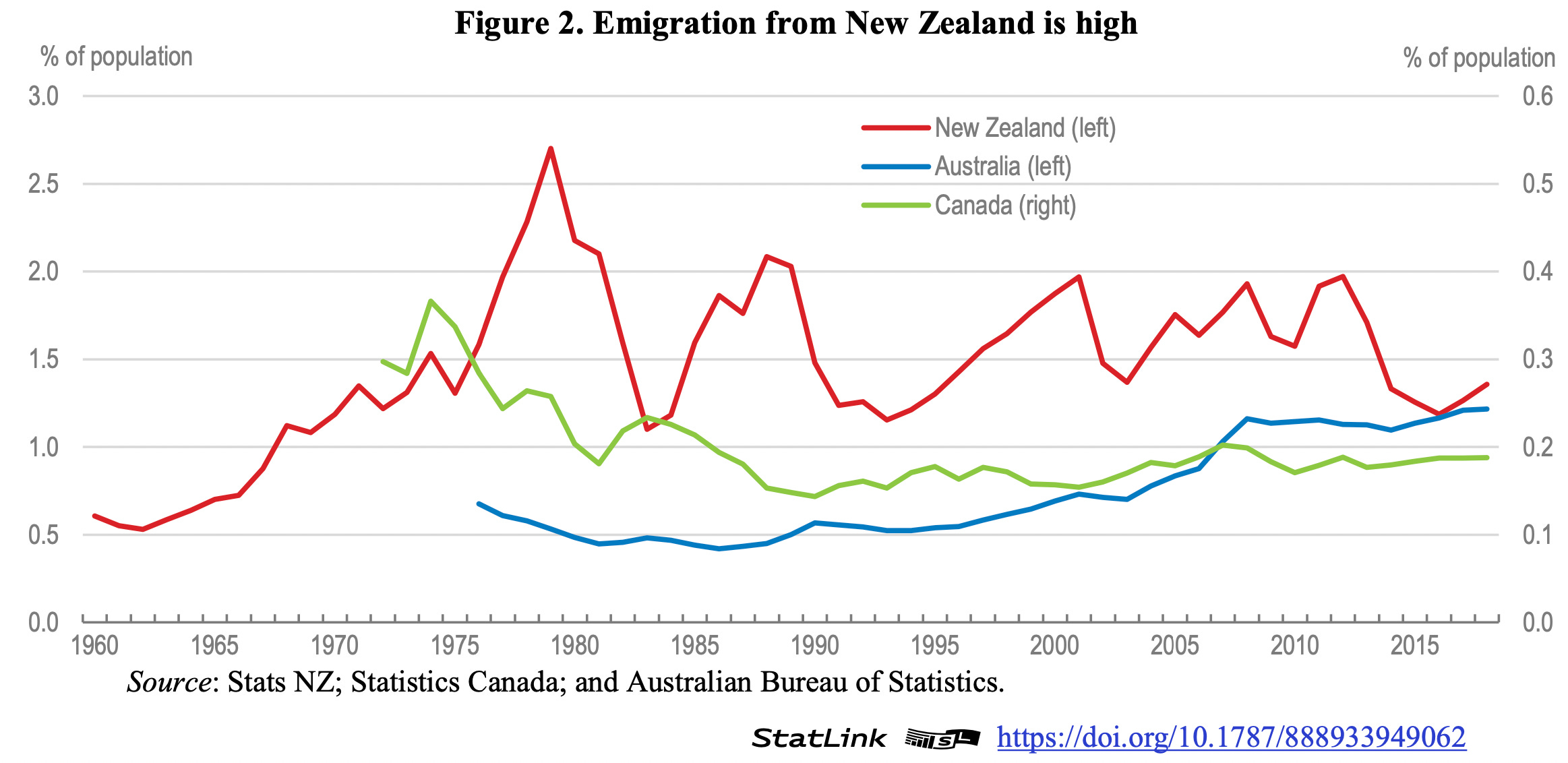

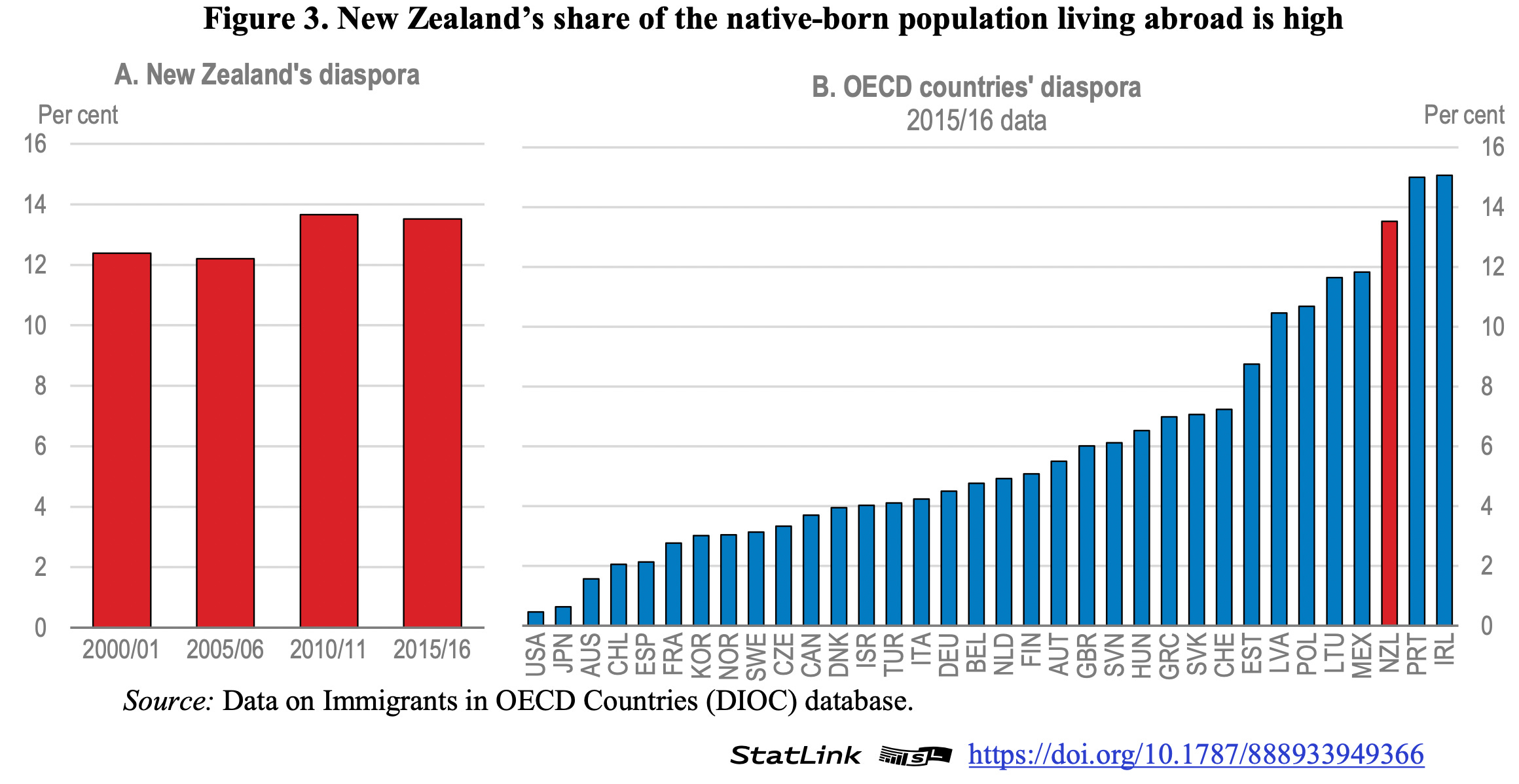

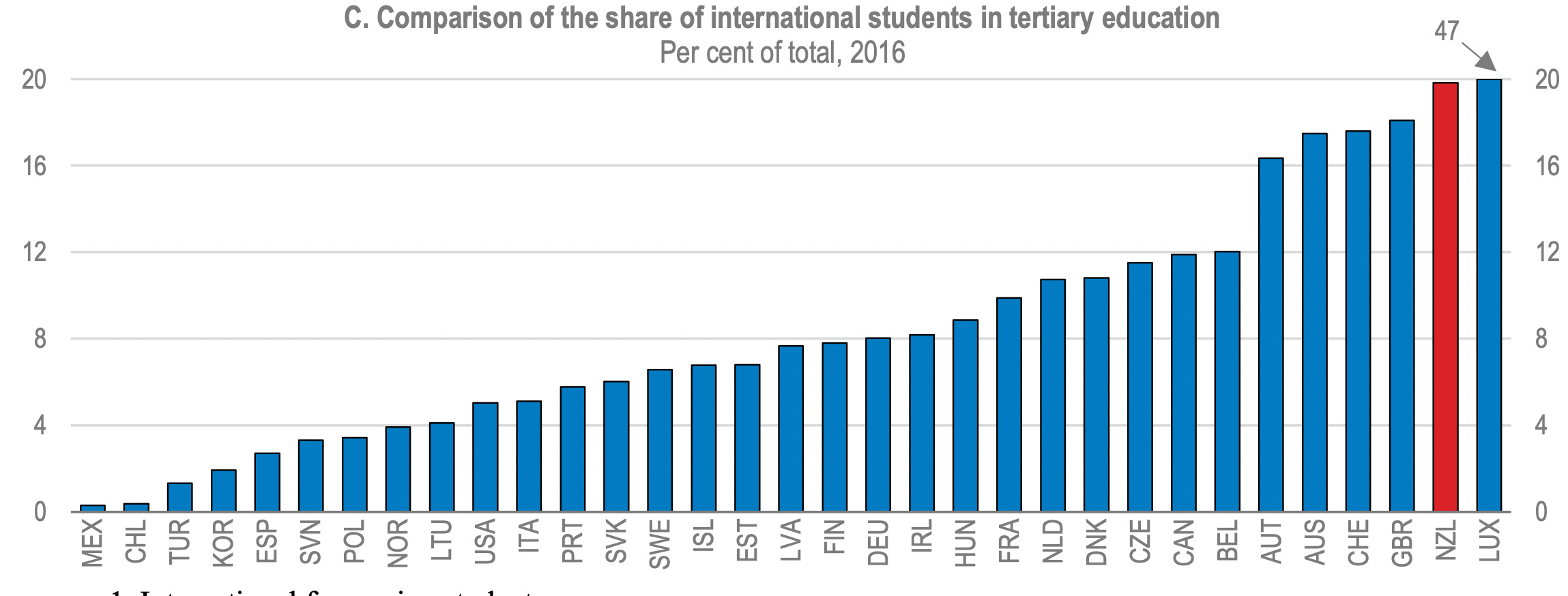

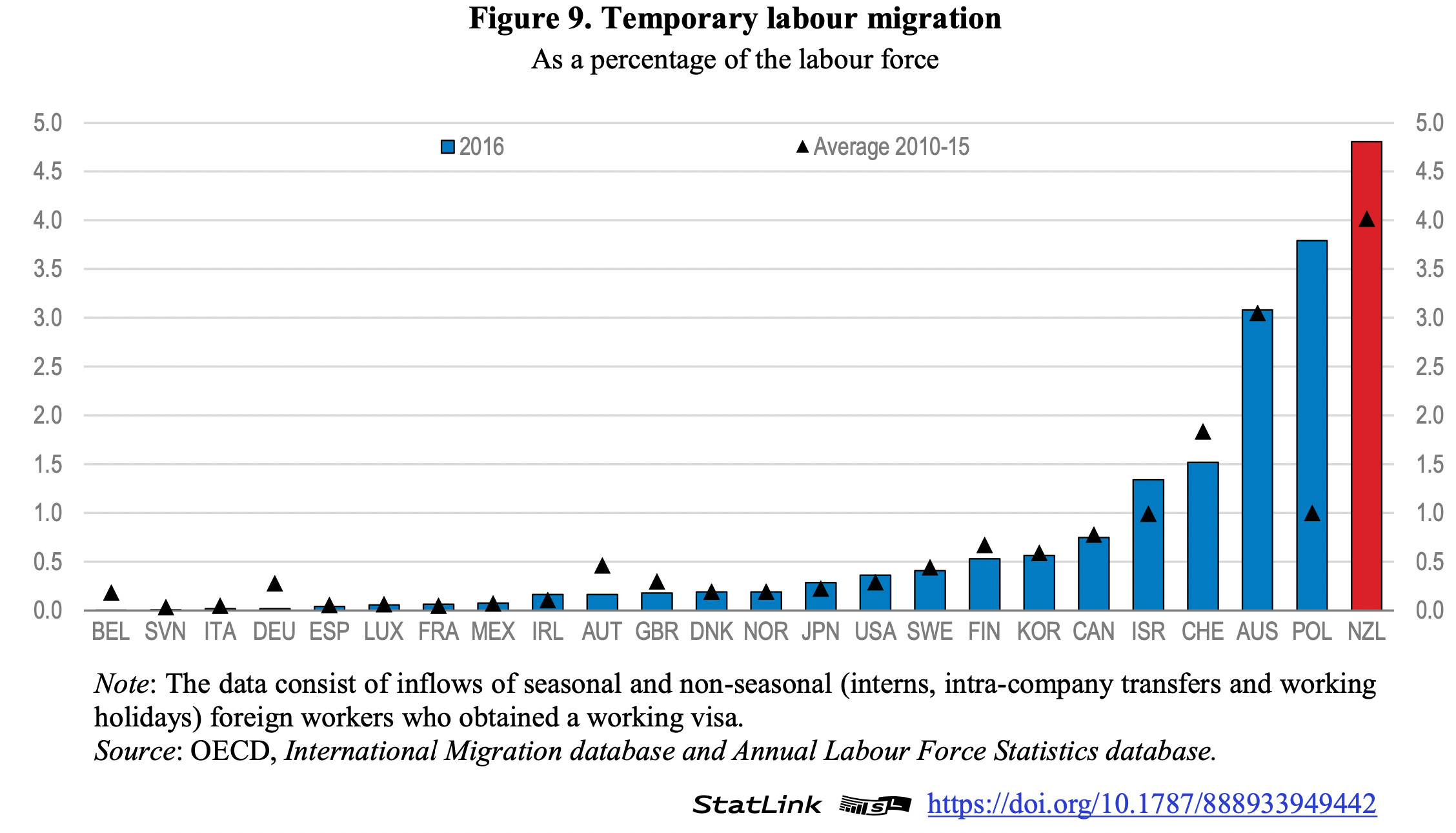

Here’s the charts from an OECD paper from 2019 titled ‘Improving wellbeing through migration’. It shows how our economy had the highest use of temporary migrant labour in the developed world prior to Covid and one of the highest rates of ‘leaching’ of home-grown talent. The temporary labour included students, working holiday-makers and lower skilled temporary work visa holders.

We built a system that sucked in new temporary workers to replace the local ones who left because they couldn’t see a future for themselves here, given brutally high housing and other costs. This system only ‘works’ for those who have already captured the unearned, leveraged and tax-free gains on residential land values.

The idea was that the Government would use Covid as ‘system reset’ opportunity to force businesses to go ‘cold turkey’ on the cheap labour, which is the oil that keeps the badly-designed and tuned economic engine running.

But a system-reset requires investment

The missing link in the theory is investment. Small businesses would need to invest in technology, consolidation, training and new management systems to increase output with the same number of workers. That requires a combination of their own investment and central and local government investment in infrastructure. That investment is desperately needed. For 30 years, Aotearoa-NZ’s households and businesses chose to invest in residential land, rather than in businesses. Governments of both flavours also chose low taxes and no taxes on leveraged gains in residential land values because that makes people on relatively low wages (who have high living costs and own homes) feel wealthy and keeping voting in Governments.

Households and businesses know the choices they have. They could invest in R&D, technology and training or M&A to make their businesses more productive. But they know that investing in leveraged residential land is vastly more profitable and vastly less risky because the Government has pledged (and shown) repeatedly that its main priority is protecting and enhancing those unearned gains in owner-occupied residential land prices. Those assurances and the lack of a tax on these gains has made Aotearoa-NZ the fastest-appreciating and most unaffordable housing market in the world in the last 20 years. Those who say our market is just as bad as others who do have capital gains taxes are just plain wrong. The outsized fall in our market since interest rates started rising also shows that.

Don’t expect a better engine without a rebuild

No party anywhere near Government, including Labour and the Greens, has ever pledged to tax owner-occupied land price appreciation. Attempts to tax capital gains beyond the family home failed to win support of median voters and is now embedded so deeply as a ‘third rail’ in politics that the most popular politician in our recent history, Jacinda Ardern, pledged never to try again in her political lifetime. The best the current Labour Government has been able to do is try to throw some sand in the gears of rental property investors through extending the bright line test for property traders, ringfencing landlords’ losses and removing interest deductibility for tax purposes.

But even those measures do not have a social license. The Opposition Leader, Christopher Luxon, has pledged to reverse all of those tax moves and is ahead in the polls. His own choices as an investor, despite his self-described success as a business operator, has been to buy rental properties. Businesses and households know the lay of the land.

The incentives are all there to invest in residential land, for both small and big businesses. The fastest-growing and newest source of wealth on the NZX in the last decade has been the listing and rise of retirement home operators such as Ryman Healthcare, which are essentially plays on tax-free capital gains on residential land values as they buy land, keep the gains, and sell services to the beneficiaries of those tax-free gains. Most small businesses would not survive long without the backstop of continued rises in land values pumping up the equity that can be used in the down years to bolster retirement nest eggs.

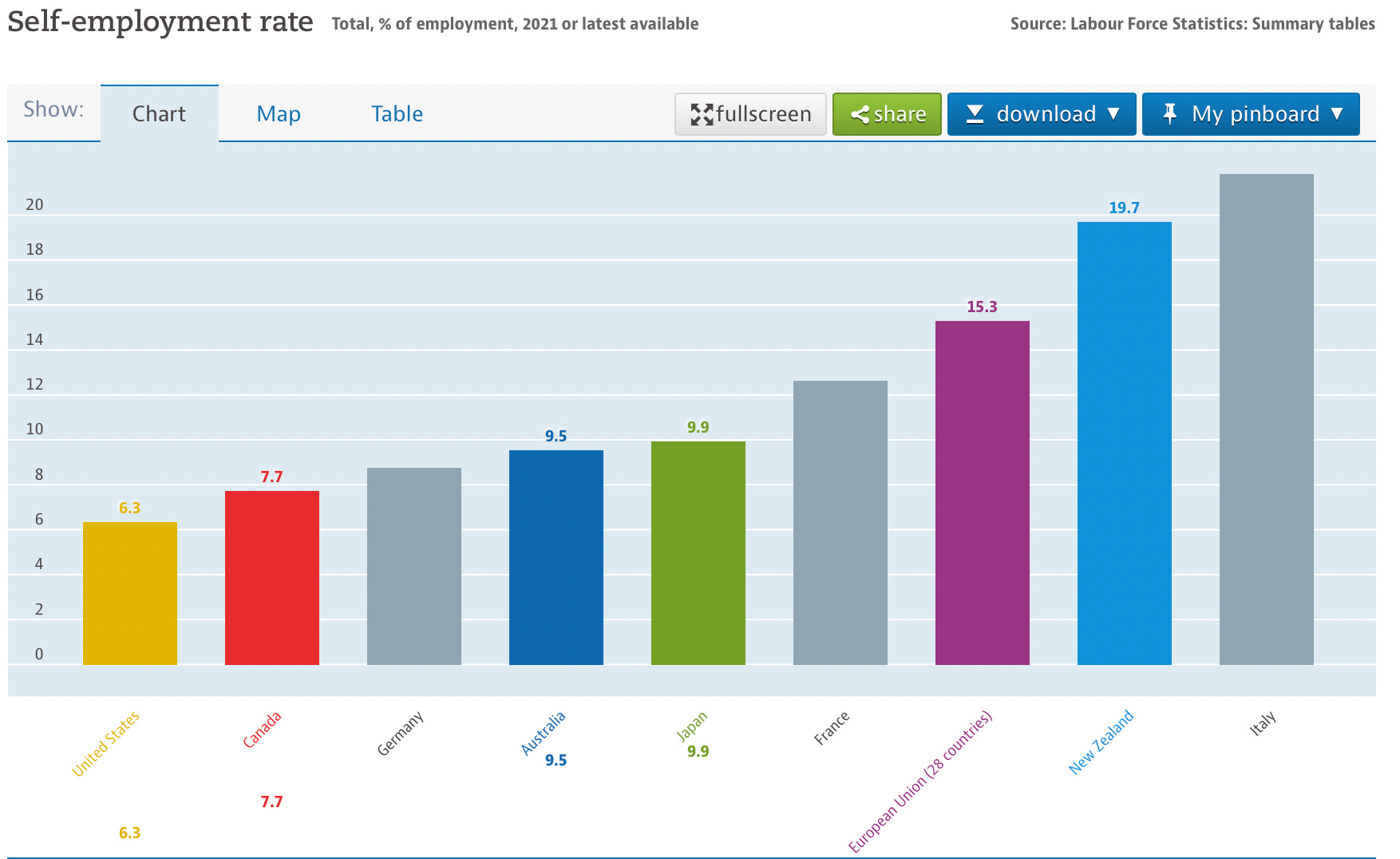

It’s one reason why we have one of the highest small-business-ownership rates and self-employment rates in the world. Our rate is more than twice that of Australia and three times that of the United States. Both have capital gains taxes and effectively incentivise the alternative of business investment, which encourages higher R&D, technology investment and international competitiveness.

After all, why bother to invest in an outward-facing high-wage business when you can build a much bigger and less-risky nest egg for your children (who will need it to get their own homes) by investing in your own residential land. When the land under our homes earns more than our actual jobs or businesses, we shouldn’t be surprised when investors choose to sink their money in dead land, rather than active businesses or infrastructure.

A failure at the first attempt and within 103 days

This week’s decision by the Labour Government to extend exemptions for at least two to three years to the median wage minimum for temporary work visa holders for construction, aged care, seafood processing and adventure tourism was announced just 102 days after the ‘rebalance’ was announced.

The attempt to go cold turkey failed after the economy had its first case of the cold sweats and violent shaking. It was always going to happen when the underlying problem of changing the incentives for Government and private sector investment remain in place.

The current machine only keeps going forward with the oil of cheap migrant workers and the rocket fuel of unearned, untaxed and leveraged gains on residential land values.

So what now?

All roads were always going to lead back to changing those investment incentives through a new tax that gives the Government the resources to invest in productivity-enhancing physical and social infrastructure. That tax would also radically change the incentives for businesses and individual investors.

As I’ve talked about in previous articles, we have to invest a lot more in infrastructure to power a burst of productivity growth that lifts real wages, real savings and the size of the economy without the need for yet more oil and petrol being pumped into a spluttering engine that is bursting a gasket and blowing black smoke.

So what type of engine rebuild might work? In my view, a Capital Gains Tax would be too politically toxic, complicated and slow to break the log jam.

The case for a residential land value tax

A much simpler, faster and more politically possible option is a simple and very-low-rate infrastructure levy or tax on residentially-zoned land values that is calculated annually from land value measures in council-maintained databases.

The Opportunities Party (TOP) has proposed such a tax in its current policy document, although it has not detailed its level or how any funds would be used.

I’d prefer to see any revenues hypothecated into a housing and climate infrastructure fund jointly administered on a region-by-region basis by central Government and councils, with the aim of using those funds to achieve affordable housing and net zero transport and housing emissions by 2050. Those responsible for the investments could target rents of less than 30% of median equivalised household disposable income and owner-occupied homes being available for five times gross disposable household income.

At current land values, a 0.5% tax on residential land values would raise an extra $6b, and effectively increase the Government’s tax rate from 30% of GDP to 32% of GDP. It could service around $120b in extra Government debt over the next 30 years with an interest rate of 5%. That would increase Aotearoa-NZ’s net debt from around 30% of GDP to 40-50% of GDP by 2050, depending on the interest rates and economic growth rates. That would still be significantly lower than net debt levels for other countries with similar economies and credit ratings such as Australia, Britain, Canada and the United States. They are all expected to have debt levels of 50-100% of GDP over the next 30 years.

I would also suggest a higher multiples for the land tax for serviced ready-to-build and unoccupied land, and zoned-but-not-occupied land to ensure land bankers release land much faster and repay some of the unearned capital gains made over the decades. You could use a similar multiple to capture the unearned gains of those owning land that benefits from public investment, including areas around rail lines, motorways and new public infrastructure such as hospitals, schools and universities.

So what would be the deal?

So it’s worth asking: in Aotearoa-NZ’s political context, how could this new settlement be found? Essentially, the two large parties would have to agree or be forced into a new consensus, which would be similar to the ones National and Labour effectively agreed from the early 1990s until today. They include:

no messing with the age of eligibility for NZ Super of 65;

no means-testing of NZ Super;

indexing NZ Super for a couple to 66% of the average weekly wage;

creating an independent inflation-targeting central bank to keep inflation around 1-3%;

leaving borders mostly tax and tariff-free; and,

keeping Government taxation and central Government net debt around 30% of GDP.

Under MMP, being forced into a new consensus would require one or both of the balance-of-power parties to dangle an affordable housing and climate infrastructure levy in front of both parties as the price of power. Te Pāti Māori and TOP would be the most obvious candidates for that, potentially in tandem.

I welcome paid subscribers’ views, suggestions and challenges in the comments below. Also: do you want this one opened up early?

Ka kite ano

Bernard

Share this post