TLDR and TLDL: The Reserve Bank publishes its quarterly Monetary Policy Statement this Wednesday afternoon with the full bells and whistles of a new set of forecasts and a news conference. Borrowers, savers and the entire political economy should pay attention to see if the bank keeps its very ‘dovish’ view. I think it will and should, but any wavering and worrying about inflation might see mortgage rates rise.

Up until now, the central bank has signalled a very loose stance with a near-zero-percent Official Cash Rate (OCR) for the forseeable future and kept its post-Covid plan to buy $100b worth of Government bonds by mid next year. But financial markets are seeing a warming economy and rising inflation risks forcing a rise in the OCR from midway through 2022. They’re looking for some sort of signal of rising interest rates in the bank’s statements and forecasts. The main focus will be on how temporary the Reserve Bank sees an expected spike in inflation next year.

Central banks overseas have held their nerve and told markets they see it as transitory and will want to see the ‘whites of the eyes’ of inflation well above 2% before they pull the trigger. They don’t want to make the same mistakes made from 2009 to 2016 or so when they all acted too early and had to reverse little rate hikes, leading to a decade of inflation below the 2% level.

The US Federal Reserve and the Reserve Bank of Australia have gone as far as saying they’re now targeting average inflation over the longer run and want a decade of inflation over that 2% level to compensate for the decade under 2%. Our Reserve Bank hasn’t gone that far, but is also pursuing a ‘least regrets’ policy of keeping policy loose until it’s clear capacity is all used up and the economy is really generating inflation.

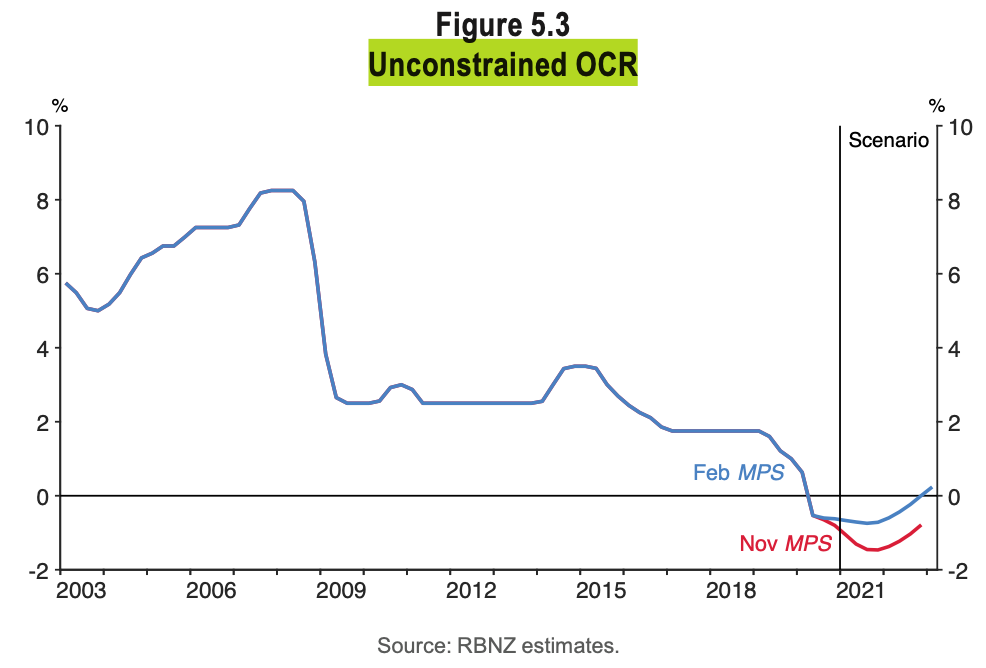

The key thing to watch will be the Reserve Bank’s comments about whether it will scale back or extend its $100b QE programme, and what it does with its ‘unconstrained OCR’ forecast track (February’s forecast below). This measure includes an unspecified combination of the OCR and the effects of the QE. The Reserve Bank announced no change to its monetary policy stance in February from November, but actually lifted the unconstrained OCR track, effectively showing a slight tightening.

This will be the chart to watch again. The Reserve Bank could easily say it is leaving policy unchanged, which is technically correct, but lift the unconstrained track to indicate it will tolerate higher longer term interest rates.

‘See off the nervous nellies’

In my view, the Reserve Bank should do what the Fed and RBA are doing: hold its nerve and wait until it sees inflation over 2% for a considerable period. It needs to rev the economy hard to blow the cobwebs out of the engine and get it nice and hot so we can get ‘rev counter’ of interest rates sustainably up to more normal levels sooner, rather than later. We have had an OCR below 3.5% for 12 years when the Reserve Bank has seen the ‘neutral’ rate above that for all that period. The risk is that investors start believing a 0.25% OCR is normal and ‘bake in’ that level to their investment and income assumptions.

There are plenty of nervous nellies calling for rate hikes now. I have a different view, which is that structural deflation from the appification of the services sector and very weak labour power will lock in these unnaturally low levels of inflation and interest rates, Japanese-style, without a real burst of hotter-than-normal activity driven by fiscal and monetary policy. We have to break out of this trap with the foot to the floor for longer.

Tell us what you think and what questions you’d like asked at Wednesday’s news conference in the comments below.

What do you want to know?

The other things I’m watching at the moment and looking at doing more on are: the Government’s review of Working for Families and the Accommodation Supplement (see more on that below), New Zealand’s FTA talks with the UK and the EU (it seems a 15 year-phase in of meat tariff reduction is now likely), the ins and outs of the social insurance scheme now being worked on, the ongoing migration review, and the future for a digital central bank currency here and overseas.

Your views and suggested questions? Comments below please.

Scoops and news breaking this morning

Elsewhere, briefly in our political economy

In the global political economy

Longer reads

Useful speeches and reports

Notable other views

Threads worth unravelling

Chart of the day

Some fun things

The sun rose in Wellington at 7.30 am and will rise tomorrow at 7.31 am.

Share this post