TL;DR: Bank economists last night firmed up their forecasts for an Official Cash Rate as high as 6.0% before the election after judging Budget 2023 to be more inflationary and generating more borrowing than they expected.

Ratings agency Standard & Poor’s warned overnight the Budget could put Aotearoa’s AA+ sovereign credit rating under pressure, although it stopped well short of issuing any formal warning of a credit rating downgrade.

Budget 2023 was seen adding around one more 25 basis point hike to the OCR, which may (or may not) increase shorter-term fixed mortgage rates by the same amount. See more on that below.

Adrian Orr’s view on whether Finance Minister Grant Robertson was fiscally loose yesterday will be crucial next Wednesday when the Reserve Bank Governor is expected to unveil another 25 basis point hike in the Official Cash Rate to 5.5%, and say whether any further fiscal policy stimulus is forcing him to tighten even more.

Economists are now asking if the central bank will have to hike by 50 basis points next week, and/or do one or two more rate hikes in July or August. The Reserve Bank’s October 4 OCR decision and statement just 10 days before the election is now shaping up as a crucial event in our political economy. Median voters in the suburbs getting ready to vote as they re-fix their mortgages will be watching with extra interest.1

Paying subscribers can see more detail, charts and analysis below the paywall fold and in the podcast above. (Updated. I’ve decided in advance to open this up to all because the Budget is such a big thing in the public interest. Thanks again in advance to the paying subscribers who support the journalism I do in the public interest on housing unaffordability, climate change inaction and poverty reduction.)

Elsewhere in the news overnight:

National said it would put the $5 prescription fee back on and not extend subsidies for childcare to young couples with two year olds, falling into two of Labour’s traps set yesterday;

Wellington Police arrested a resident of Loafers Lodge and charged him with two counts of arson over the fire that killed at least six of his fellow residents on Tuesday morning;

Chances of a US debt default reduced overnight as Democrats and Republicans expressed confidence they could do a deal to lift the debt ceiling, which boosted global stock prices; and,

Geopolitical tensions between China and Australia cooled overnight, with China removing a ban on Australian timber imports and talking about inviting its PM Anthony Albanese to visit China, which may increase the chances of a visit to Beijing by PM Chris Hipkins, possibly as early as July.

I also put these news items out in truncated form just after 6 am for paying subscribers via Chat on the Substack app, where the chat between subscribers (and me) continues. Download the app and upgrade to being a paying subscriber to join. Also, paying subscribers can comment in my weekly Ask Me Anything session at midday today, and join our weekly news roundup webinar we call The Hoon at 5 pm for an hour. It is released in recorded form as a podcast tomorrow morning.

Bank economists say Budget 2023 was more inflationary

Bank economists have firmed up their forecasts for two or three more official cash rate hikes to as high as 6.0% after Budget 2023’s inflationary stimulus and its bond borrowing programmes were higher than they expected.

Credit ratings agency Standard & Poors, but not Moody’s, also described the Budget as ‘fiscally expansionary’ and said it could “erode headroom for the sovereign ratings on New Zealand.”

Budget 2023 was seen adding around one more 25 basis point hike to the OCR, which may (or may not) increase shorter-term fixed mortgage rates by the same amount. My view is banks are currently competing hard for market share to revive lending growth, which may mean they hold back from hiking their discounted fixed mortgage rates in coming months, although floating mortgage rates would be more likely to be hiked if the OCR is hiked.

There’s a selection below of reaction from bank and other economists to yesterday’s Budget, which Treasury judged would be more inflationary in the next year, but would detract from inflation over the full four-year outlook presented in Budget 2023.

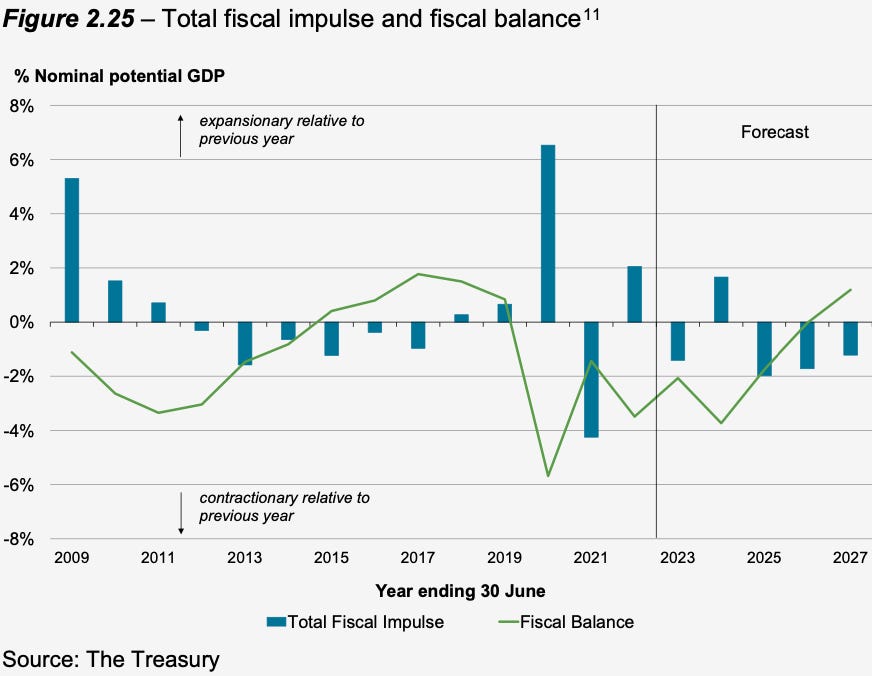

But first, here’s the Treasury’s comments and chart in the Budget Economic and Fiscal Update (BEFU) (pages 14, 59) below (bolding mine), showing the extent of the Government’s ‘fiscal impulse’ over the next four years. I’ve also included audio in the podcast above2 of my exchange with Grant Robertson in the Budget lockup news conference about whether the Government had worsened inflation and interest rate pressures. He downplayed the idea. I’ll ask Adrian Orr the same question in next Wednesday’s news conference in Wellington, which I’ll attend. I welcome any other questions you’d like put in the comments below.

The total fiscal impulse implies that, over the forecast period as a whole, fiscal policy settings are expected to be contractionary. This means fiscal policy settings will suppress aggregate demand and inflation pressure over the forecast period as a whole. However, fiscal policy settings are expected to be less contractionary than was forecast in the Half Year Update3. Fiscal policy settings are expected to be expansionary in the 2023/24 fiscal year (1.7% of nominal potential GDP), meaning fiscal policy will be supporting aggregate demand and inflation pressure in that year. (Page 14)

A stronger fiscal balance forecast for 2022/23, relative to the Half Year Update, also exacerbates the difference between the two years, leading to a more positive impulse than would otherwise be the case. The fiscal balance is forecast to improve from 2024/25 and through the remainder of the forecast period, with a positive fiscal balance expected in 2026/27 (two years later than forecast at the Half Year Update). As a result, the fiscal impulse is forecast to be negative (contractionary) from 2024/25 and through the remainder of the forecast period. Treasury BEFU. Page 59

What the bank economists said last night

ANZ’s economists, who increased their peak OCR forecast to 5.75% from 5.50% earlier this week, said Budget 2023’s borrowing programme was twice as large as they expected and the extra 1% of GDP stimulus implied in the Budget had been estimated previously by Treasury as enough to cause a corresponding 30 basis point increase in the OCR to offset the inflation impact. Here’s their comment from the note (bolding mine):

“The additional fiscal stimulus represents more pressure on CPI inflation and therefore an upside risk to the OCR outlook.

“The RBNZ won’t have to wait long to bake today’s information into its outlook – the May Monetary Policy Statement (MPS) is next Wednesday. We doubt the RBNZ will go so far as to specify precisely what fiscal settings imply for the OCR, but today’s Budget certainly adds a touch more oomph to the demand pulse, working against the broad macroeconomic slowdown the RBNZ is trying to engineer to tame inflation.” ANZ’s economists in a note issued last night.

Westpac’s economists, who lifted their OCR peak forecast to 6.0% earlier this week, wrote:

“All up, the fiscal forecasts are more expansionary than we had anticipated. As a result, the Budget will add to inflation pressures in the short term.” Westpac economists in a note.

ASB economists said the Budget’s loosening made a 50 basis point hike next week more possible, as they wrote in this note (bolding mine):

“The RBNZ would not have been overjoyed with what has been revealed to it. According to the Budget 2023 fiscal impulse, the fiscal stance is expected to exert a considerably less contractionary impact on aggregate demand over the next few years than was earlier signalled.

“The worry for the RBNZ could be that this less contractionary fiscal stance will be less effective in cooling demand and inflationary pressures in the current environment of strong demand for government services in a still-high cost environment. The RBNZ seems highly likely to follow through with at least a 25bp hike in May. We don’t see fiscal policy settings as proving an obstacle to a higher OCR in the near future, and risks of a 50bp hike in May look to have increased after the Budget.” ASB Economist Mark Smith in a note.

BNZ’s economists lifted their OCR peak forecast to 5.75% from 5.50% by July after the Budget yesterday and BNZ Market Strategist Jason Wong said this in his morning note (bolding mine):

S&P fired a warning shot, noting that NZ must deliver stronger fiscal metrics than peers because of the external vulnerabilities, adding “downward pressure on the sovereign rating could eventuate if external metrics remain weak”. Twin deficits of 6.5% of GDP on the fiscal side and 9% for the current account is not a good position for a small country like NZ to be in.

Easy fiscal policy is set to work against the RBNZ’s endeavours to weaken domestic demand, adding to the chance of a higher peak OCR rate, and BNZ Economics added in an additional 25bps to its projections, now seeing two 25bps hikes taking the OCR to 5.75% in July.

Domestic rates were higher across the board, with OIS (Overnight Index Swap) pricing for August up 10bps to 5.79%, taking its gain for the week so far to 28bps. With next week’s meeting priced at 5.55%, the market sees a 20% probability of another 50bps hike, rather than the RBNZ settling for 25bps. The swap curve showed further flattening pressure, with the 2-year rate up 17bps on the day to 5.29% and the 10-year rate up 10bps to 4.34%. BNZ Market Strategist Jason Wong in a note emailed to clients this morning.

The bottom line for Budget 2023 is the 17 basis points rise in wholesale interest rates and what bank CEOs will do about that

That 17 basis points of rises in the two-year swaps rate yesterday is the ‘meaning’ from Budget 2023 for median voters with mortgages about to be refixed ahead of the election on October 14. If banks choose to pass it on with higher fixed mortgage rates, then it will hurt Labour’s chances of re-election.

Perhaps ironically, the CEOs of New Zealand’s big four Australian-owned banks are now in the position to either ‘punish’ the Government by passing on higher mortgage rates to engineer a change of Government to one they might like better, or they can choose to keep Labour sweet ahead of a looming market study next year by not passing on the increases in wholesale rates and the OCR.

This is what ‘realpolitik’ looks like in our political economy dominated by a housing market with bits tacked on, where the political calculus revolves around the needs and feelings of median-voting young families with mortgages in the suburbs of the big cities and provincial towns. And it’s all because these median voters cannot kick their addiction to leveraged and tax-free gains on residential land, and therefore won’t (or can’t) choose the alternative of taxing those gains and having higher public debt toinvest more in public infrastructure and services, R&D and business investment that would improve our productivity, real wages, health, housing affordability and climate emissions, and reduce poverty.

Bank CEOs and median voters will decide what Budget 2023 means for the result on October 14

The net result from Budget 2023 for this relatively small group of around 100,000 voters of the last day’s ‘action’ in the political economy is that Labour pulled the following ‘rabbits’ out of the hat for them:

the end of $5 prescription charges for all the medications they need for themselves and their kids;

$130 a week worth of subsidies to put their kids into childcare for an extra year from the age of two, which might help them return to work earlier to earn more cash to pay for higher mortgage costs;

possibly a little extra in Government contributions to their KiwiSaver for those parents who took paid parental leave;

free bus and train fares for their kids aged up to 12, and half-price fares for those up to 25 with a community services card; and,

possible extra subsidies to insulate and heat the homes they just bought;

an extension for their kids in school of the free-lunch programme to the end of next year, estimated to be worth up to $60 a week for some parents.

On the other side of the equation, National fell into the traps Labour carefully laid yesterday by promising to:

reverse the removal of the $5 fee;

not discount bus fares; and,

not extend childcare subsidies.

The danger for Labour and the hope for National is that:

the Reserve Bank hikes the OCR much more than expected next week (50 bps rather than 25 bps);

Adrian Orr hikes one or two more times before the election (the next OCR decisions are on July 12, August 16 with a news conference and October 4);

Adrian Orr specifically blames a loosening of Budget policy by Labour for the hikes; and,

the bank CEOs choose to pull the trigger to put Labour out of Government by passing on the rate hikes into much higher fixed mortgage rates.

A time for spectators and manifestos

Young renters, particularly single ones, are just spectators at this point.

They may be better off choosing to spend their time during the election campaign perusing job listings in Australia and the offers for Trans-Tasman flights on Grabaseat and Jetstar.

Unless Chris Hipkins and Grant Robertson choose the change the landscape by proposing in Labour’s manifesto a wealth tax and a massive inter-generational investment programme in climate-friendly and affordable housing and transport to reduce housing costs, cut emissions more deeply and slash poverty rates.

My current expectation is there is little-to-no-hope Hipkins will take those electoral risks in a political environment where MMP and low-target policies have locked Aotearoa into our ‘churn and burn’ economy of low public debt, low taxes, low investment, low productivity and low wages enabled by no capital gains tax, high migration, high house prices and high rents.

I look forward to hearing from you in the Ask Me Anything at midday and in the Hoon at 5pm.

Ka kite ano

Bernard

Please forgive the pun. I’m a financial and economic journalist. I have no choice. It was too obvious to ignore. Also, I co-founded Interest.co.nz, so it just fell out onto my keyboard. Bite me.

Sorry about the audio quality. It is a big echo chamber in the Beehive Banquet Hall…

Treasury forecast in December’s HYEFU (Page 54) there would be an impulse of 0.8% of nominal potential GDP in 2023/24. That means yesterday’s forecast for a 1.7% impulse implies the ‘extra’ inflationary pressure in yesterday’s Budget was worth about 1.0% of GDP. Treasury has previously said every one percentage point of ‘impulse’ would in theory require about 30 basis points of monetary policy tightening to offset the inflation impact.