TLDR & TLDL: The housing market isn’t cooling nearly as much as policymakers and politicians expected after they tightened lending rules and announced the removal of tax deductibility for the homes landlords already own.

It’s still early days, but sales volumes haven’t slowed much at all in the two months since the policy changes and inflation in the last three months was still running at an annualised rate of over 20%. See more commentary below.

Elsewhere locally overnight

The South Island’s State Highway One reopened just before midnight last night when the Ashburton Bridge started taking traffic again. (The Press)

Later this morning, the Victorian Government is expected to announce the extension for another week of Melbourne’s seven-day lockdown after four or five new community cases of the Indian variant were discovered after just fleeting contact. (ABC)

Politik’s Richard Harman reports this morning in his subscription newsletter that Judith Collins appears to have engineered the resignation of Nick Smith by telling him about an apparent upcoming news report on his verbal altercation last year, which Collins had known about from the beginning. (Politik-$$$)

A $100m bid by the Government and the Auckland Council to TeamNZ to host the next America’s Cup has been rejected. (NZ Herald)

Overseas, overnight:

Oil prices rose 3% to a two-year high overnight after Opec + agreed on only slow increases in oil production. (CNBC)

Eurozone inflation rose to a two-year high of 2%, which is at the European Central Bank’s target already and above market expectations for 1.9% inflation, increasing pressure on the ECB to wind back its money-printing programme. (Reuters)

Australia is set to launch a WTO complaint against China over wine tarriffs, giving New Zealand the chance to repeat its seconding of Australia’s barley complaint. (The Australian)

The New South Wales Government used an accounting trick to shift billions of dollars of rail costs into a shell company to avoid a credit rating downgrade last year. (SMH’s Adele Ferguson)

Iron ore prices rose over US$200 a tonne again overnight on reports China’s attempts to slow demand from steel mills was failing. That’s great news for the Australian economy and Government, which has posted surpluses in the last two months because of taxes from iron ore mining. (Mining.com)

A ransomware attack that disrupted production by the biggest meat processor in America and Australia, JBS, came from Russia, the White House said overnight. (Reuters)

Wairoa inflation over 50%

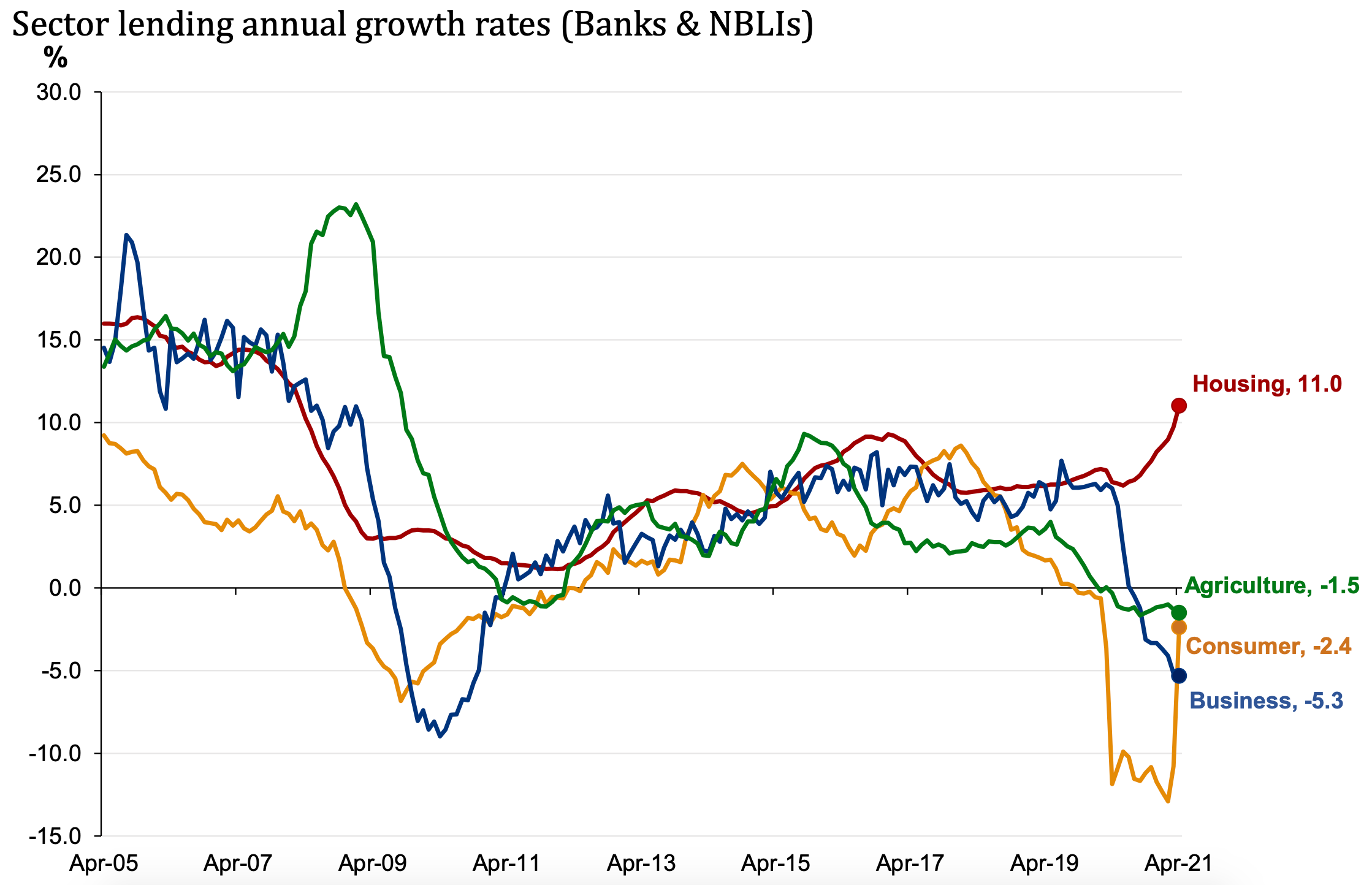

CoreLogic reported last night house value inflation nationally of 7.7% in the three months to the end of May, despite the March 1 reimposition of LVR restrictions, the shock announcement on March 23 tax deductibility removal for landlords’ existing homes and the May 1 increase in deposit requirements for landlord buyers of existing homes to 40% from 30%.

I spoke to CoreLogic’s Head of Research Nick Goodall last night (audio above) and he said the initial signs were still stronger than implied in Treasury’s forecast on May 21 of annual house price inflation slowing to 0.9% by the middle of next year and in the Reserve Bank’s forcast last week of inflation slowing to 0.4% by June 2022.

Even in the last three months, house price inflation is already running much hotter than the Reserve Bank and Treasury have forecast. Just last week, the Reserve Bank saw house price inflation of 5.5% in the June quarter. That inflation has already been achieved with a third of the quarter yet to go.

So far, the CoreLogic index has risen 5.6% since the end of March, 15% since the late November announcements from Finance Minister Grant Robertson of a ‘demand and supply policy reset’ and the imposition of a sustainable house prices mandate on the Reserve Bank. They are up 23% since the arrival of Covid-19. The value of the housing market has risen by $278b to $1.5 trillion since the start of Covid.

The numbers continue to astonish. Wellington’s average house value rose over $1m for the first time in May and was up 27% from a year ago. Annual house price inflation in Napier, Palmerston North, Kapiti Coast, Whanganui and Gisborne were all over 30%. Values in Wairoa were up 52.4% from a year ago.

‘We don’t believe you any more’

Home buyers, be they first home buyers or landlords, simply don’t believe either the Reserve Bank or the Government any more when they say they’re serious about making house prices affordable, or warn that buyers might be over-extending themselves or be burnt by a rise in interest rates. Central bank Governors and Finance Ministers have cried wolf too many times over the last decade to be believable.

The voting and home buying/renting public have seen what the Reserve Bank and the Government have actually done and not done over the last decade and have stopped believing the forecasts or the reassurances. They saw the Reserve Bank and the Government act in March last year to ensure the protection of the housing market, which is now not only too big to fail but is the only tool for the Reserve Bank and Government to stimulate the economy and reassure nervous median voters and small businesses in a crisis.

The Reserve Bank slashed interest rates and promised to print $100b to boost the wealth effect of the housing market on consumers and businesses. It removed the bank restrictions on lending and then created a scheme to lend to banks at 0.25% so they could further boost housing market values. It also delayed the introduction of tougher capital requirements to ensure banks kept lending into the housing market. Reserve Bank stats show banks have lent an extra $21b into the housing market since the first lockdown.

Voters and buyers have seen the continued refusal of councils and the Government to use their balance sheets to properly fund the housing and transport infrastructure needed to build the 500,000 houses needed to deliver the supply shock that would make house prices affordable. They saw the Prime Minister promise never to introduce a capital gains tax in her political lifetime and promise not to tax wealth at the last election.

Boosting housing’s wealth effect is a feature, not a bug

Understandably, home buyers have stopped believing the ‘grown-ups’ when they say house prices could fall and that buyers and investors should abandon their ‘silly fear of missing out’ approach to the housing market. There have been so many times in the last decade when it seemed prices were totally crazy, out of whack and unsustainable, and yet rose another 20% or 50% or 100% within a few months, years or a decade.

As this ASB survey from last week shows, a net 64% of those surveyed expect house prices to rise over the next year and only once in the last two decades have those expectations wobbled. It turns out the voting and home-buying public were a much more accurate forecaster of the housing market than the Reserve Bank and the Treasury.

Briefly elsewhere in our political economy

Useful longer reads and listens

Share this post