TLDL & TLDR: Now the dust has settled, let’s look at the damage, or more importantly, to see which village was burned to save the town.

The Reserve Bank is ending its money printing programme today, having printed $53.5b to buy bonds so that even lower interest rates would create a ‘wealth effect’ that rescued the economy.

It worked perfectly, but in an instant, and with little apparent concern for those without assets, the RBNZ and the Finance Minister who signed off on the plan have destroyed what was left of the home-owning hopes of a generation, especially those (often Maori and Pasifika) youth who cannot rely on property-owning parents to help them.

Aotearoa-NZ is still in shock at what happened, and the Reserve Bank, Treasury and the Government are reluctant to acknowledge the longer-term effects on society, especially for inequality. They are still quibbling over whether the interventions in late March 2020 to unleash lending controls, to suspend higher bank capital plans and to launch a plan to print money worth 30% of GDP has actually worsened inequality.

Astonishingly, the Reserve Bank released a research paper in May saying “is not clear that lower interest rates always make wealth or income inequality worse.”

“The overall effect of monetary policy on inequality is indeterminate and depends on the strength of each channel, which may reinforce or offset each other.” RBNZ’s Jinny Leong.

Treasury is also still apparently flummoxed by what just happened and unwilling to call a spade a bladed instrument for digging holes. Secretary Caralee McLiesh told MPs in February it’s still too early to assess the full impacts of the pandemic on inequality.

“It does have flow-on effects and clearly lower interest rates is one of the drivers of higher house prices. But the overall impacts on wealth inequality are quite complex and difficult to unpack.” Treasury Secretary Caralee McLiesh in February.

This is despite Treasury advising Finance Minister Grant Robertson on March 16, seven days before the money printing programme known as LSAP (Large Scale Asset Purchases) was announced, and nine days before it started:

“LSAPs have many of the same distributional impacts as conventional monetary policy, but can raise asset prices more directly than conventional monetary policy, creating wealth inequality. However, they can also mitigate inequality by supporting employment.” Treasury advice on March 16, 2020.

The bolding is mine.

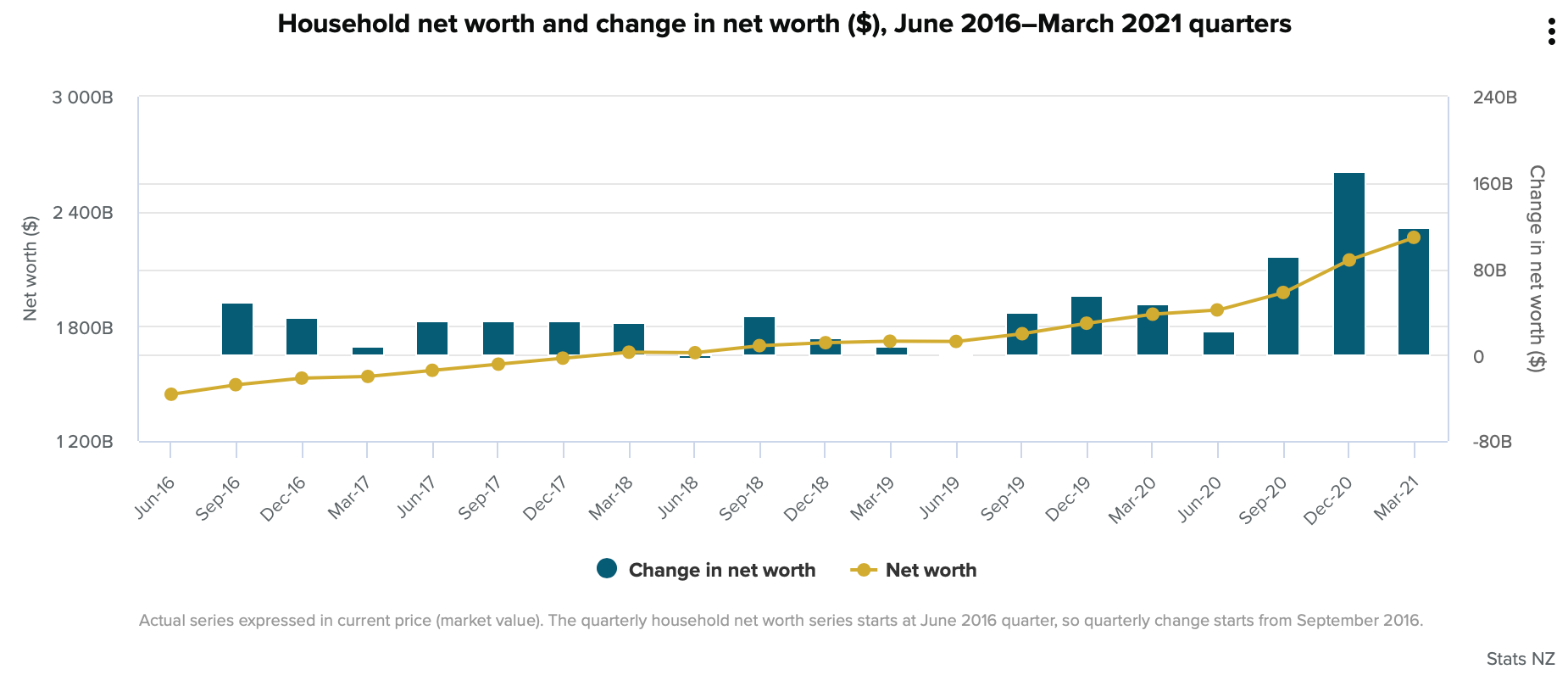

Here’s the data to prove it

They and those in the generation thinking about household formation only need look at yesterday’s new figures from Stats NZ on household wealth to understand what happened. The bolding is mine.

“Since March 2020, household net worth has increased $402 billion, nearly as large as the accumulated growth over the period June 2016 to March 2020 ($419 billion). While household loan debt has increased $16 billion from March 2020, the value of household assets has risen $417 billion.

Financial assets contributed $245 billion to the increase in household assets since March 2020, exceeding the rise from owner-occupied property ($172 billion). Financial assets of households include equity (such as shares, businesses, and investment funds), pension schemes (like KiwiSaver), and deposits at banks.

Households’ ownership of rental properties is included in the accounts as financial asset equity in businesses (residential property operators). When combining rental properties with owner-occupied property, the increases in the values of residential property accounted for about 54 percent of the household asset increase for the March 2021 year.” Stats NZ in its data release yesterday.

Just over half of the $402b increase in household net worth came from housing, which was driven almost solely by lower interest rates due to the LSAPs programme and the removal of LVR restrictions, given migration collapsed over that year and housing consents grew at a record-high pace through the year.

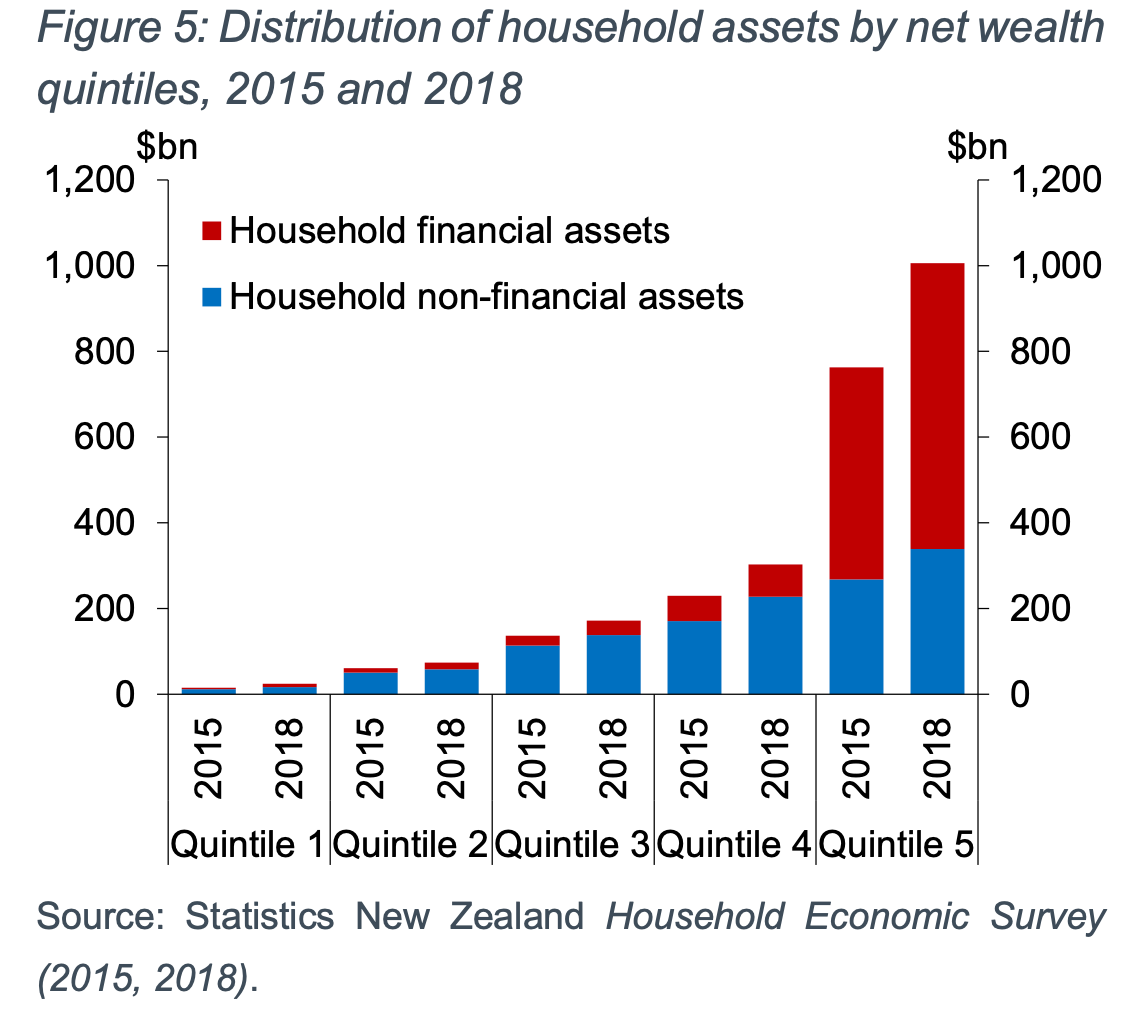

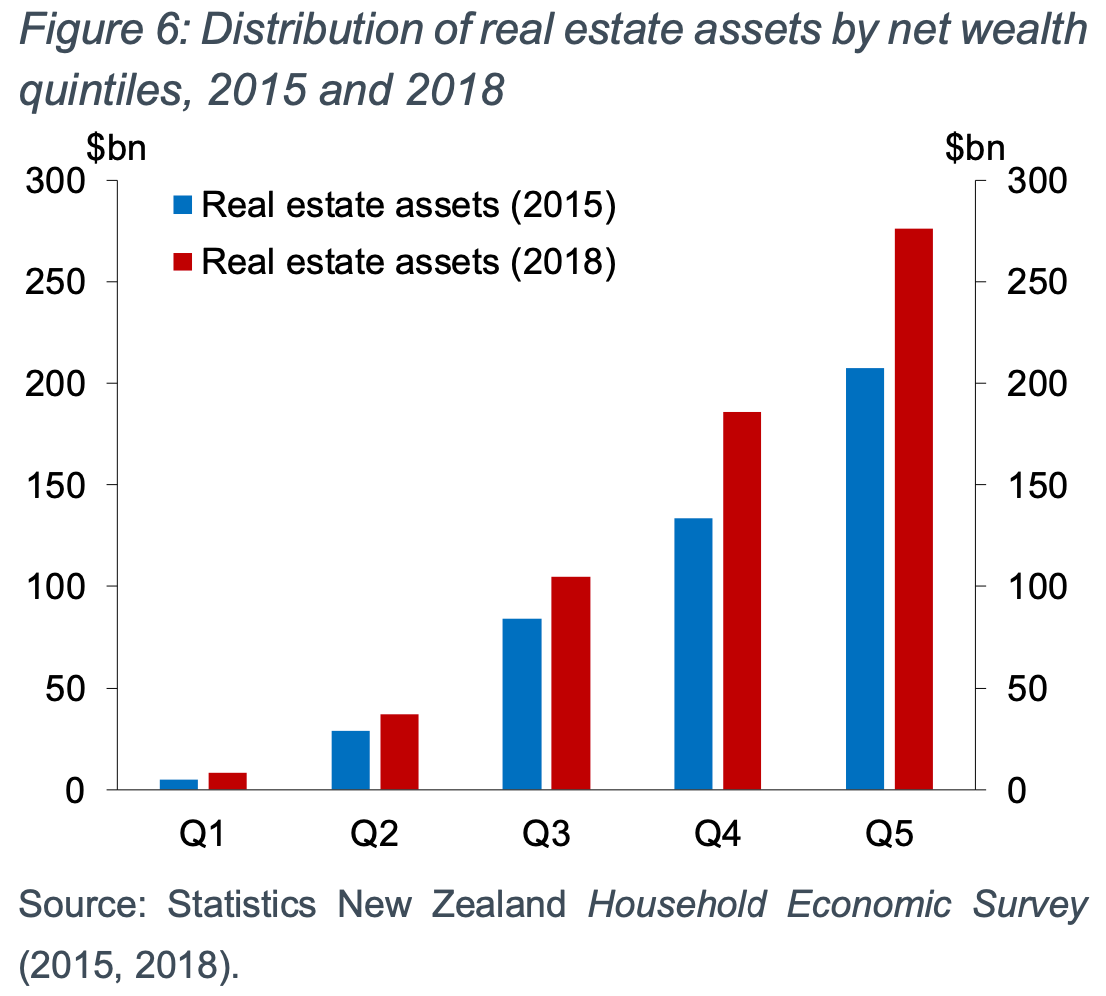

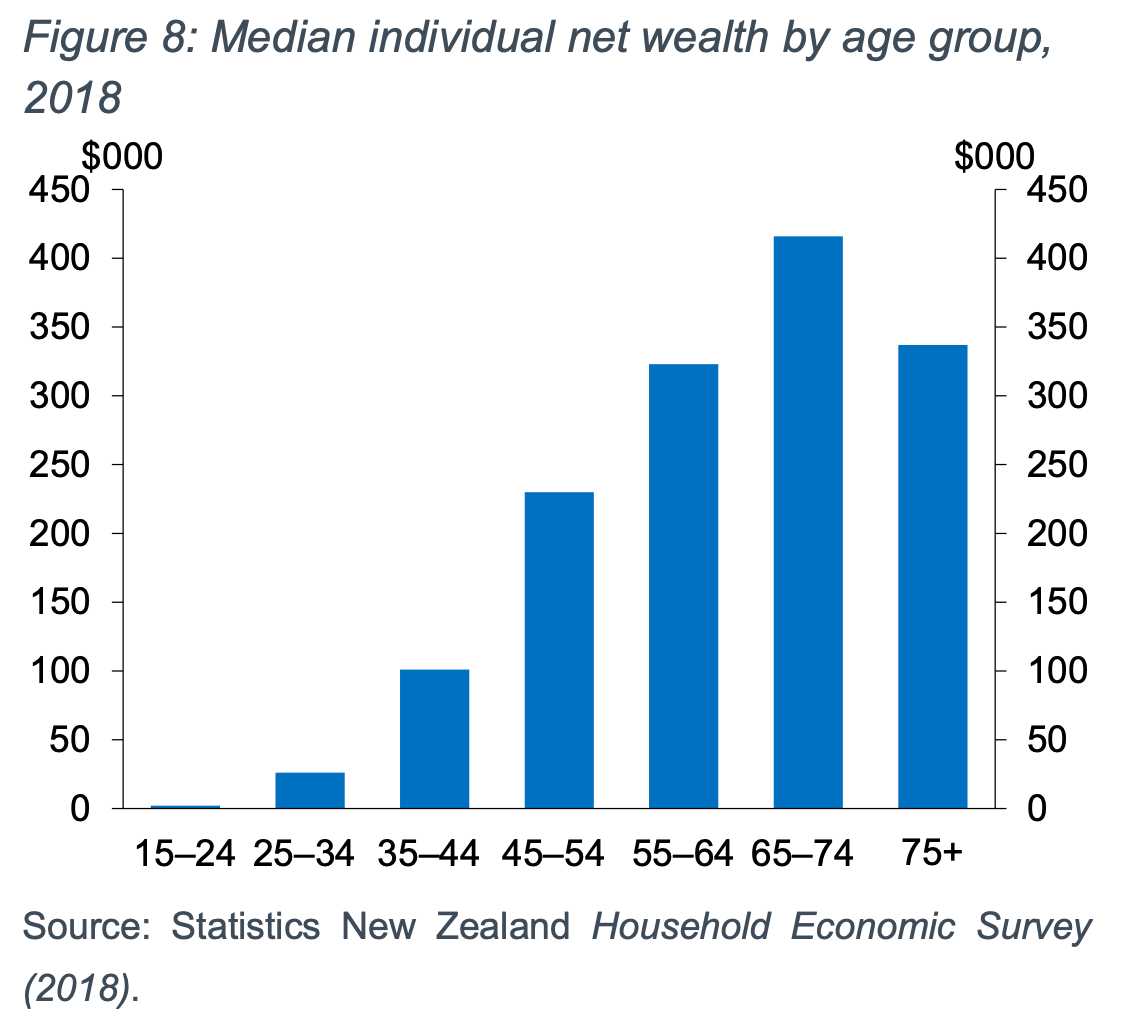

If the Reserve Bank needed any indication of what that would do to existing wealth inequality, it need only look to its own data and charts from its paper looking at whether lower interest rates worsen inequality. The quintiles represent the population broken up into 20% chunks with the richest 20% at the far right, as of 2018.

And here’s what that Covid wealth dump did to young peoples’ dreams

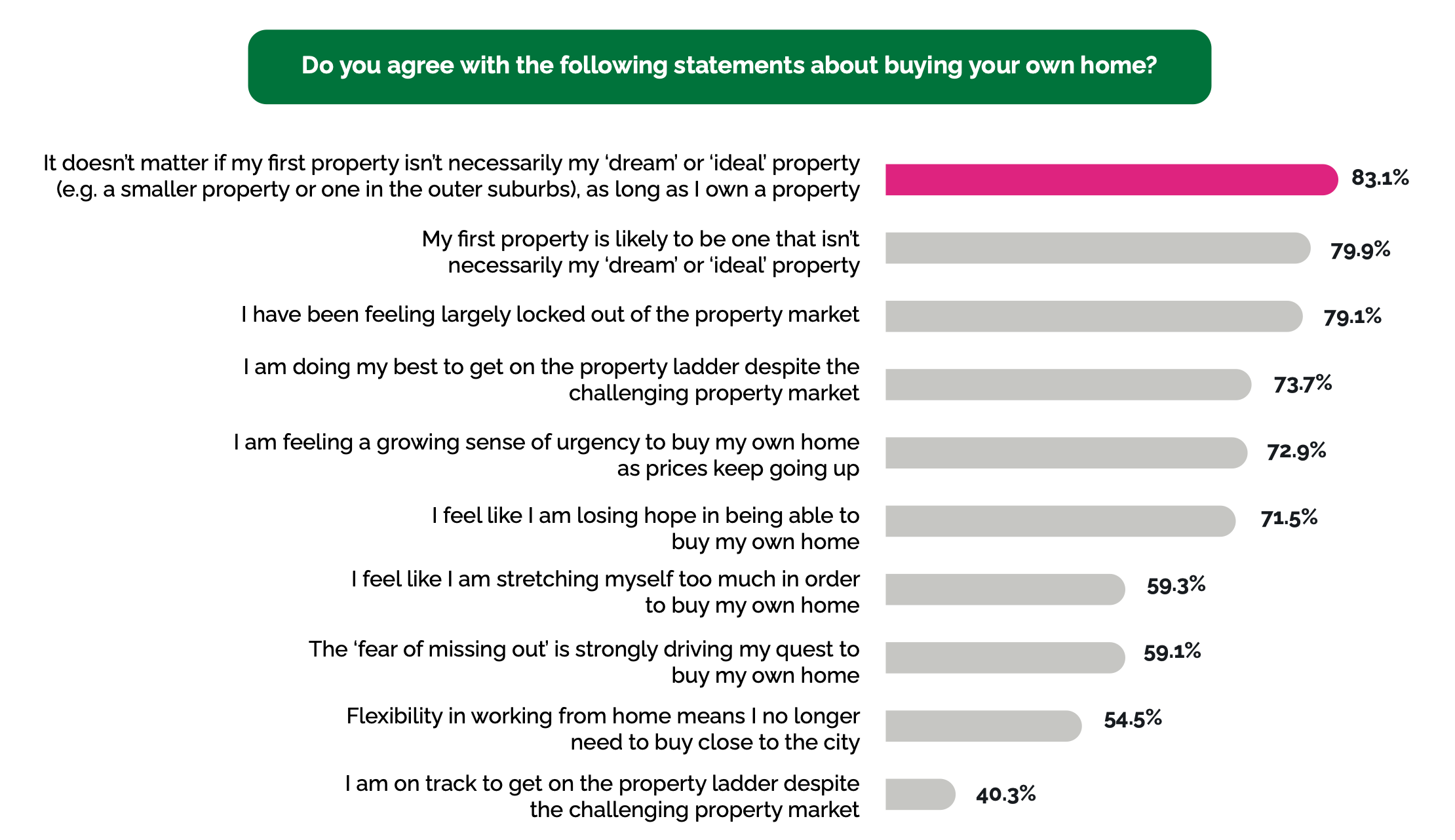

Also out yesterday, results from a poll of 500 New Zealanders in late March that showed how most now see the dream of home ownership as dead. The poll was commissioned by OneChoice and conducted by CoreData. Just over 41% of the respondents were in Gen Z (<25 years) or Gen Y (26-40 years).

It found 79% feeling locked out of the market, 72.9% feeling a ‘growing sense of urgency’ to buy a home as prices kept rising, and 71.5% feeling like they were losing hope about ever owning a home. It found 88% believed younger people were getting locked out of the housing market and 83.4% felt the dream of home ownership was no longer attainable. Just over 54% now thought the dream of home ownership was no longer relevant.

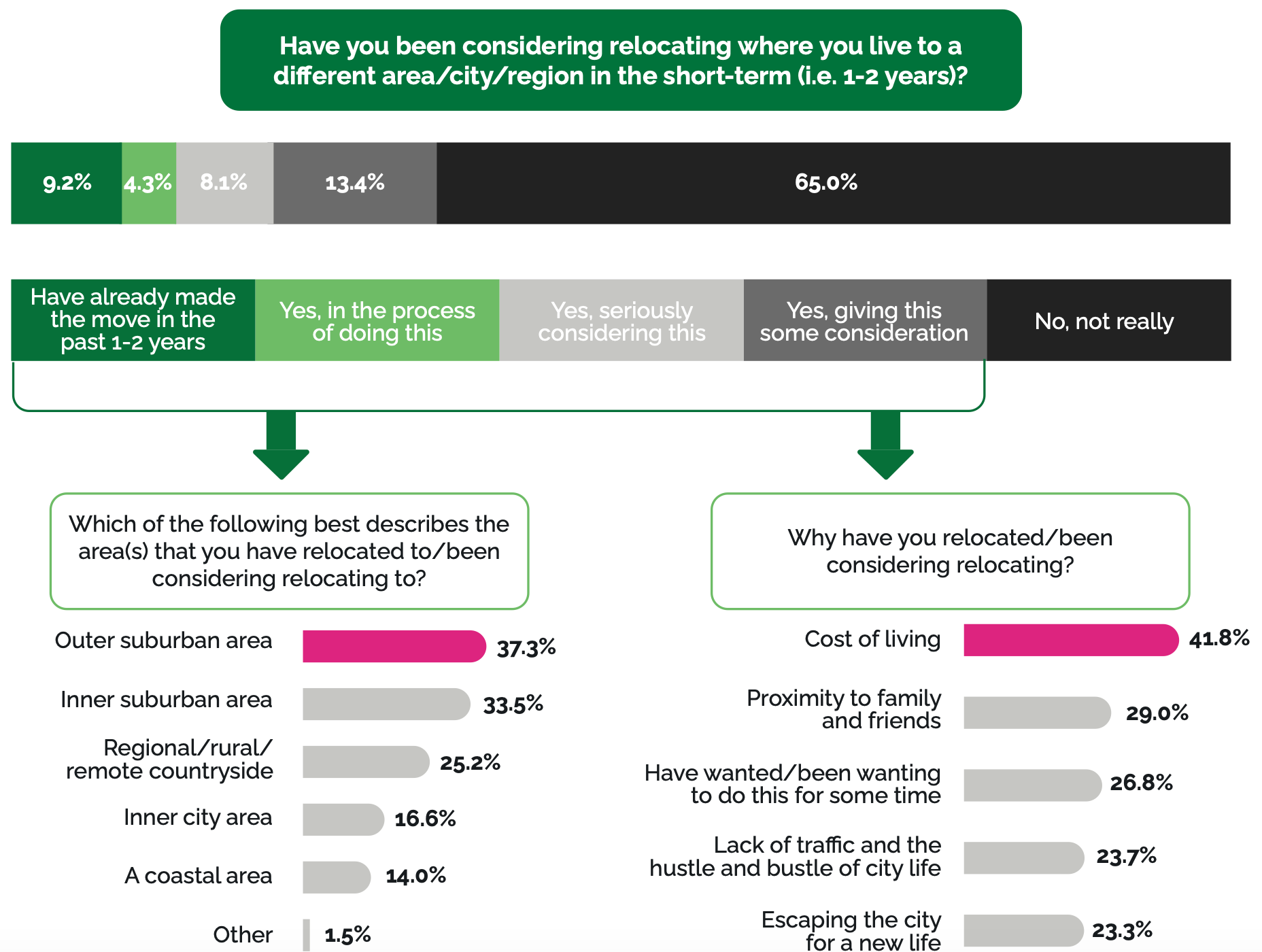

These results were reflected in views about moving, with 35% looking to move, most to outer suburban areas, and mostly because of cost of living reasons. Interestingly, 14.7% of those surveyed said they now planned to have children later because of the Covid experience, with a 30% saying that was for financial reasons. Over 60% of those surveyed who did not have children said they planned never to have any children.

My view: The political fallout has yet to really start from this deliberate public policy decision to make wealthy people even wealthier while simultaneously making it harder for the poor to get ‘on the ladder’. The Government’s decision not to more widely distribute cash grants to poor renters and beneficiaries, rather than business owners (many of whom have not repaid the cash grants and have instead bulked), will compound the backlash when it comes.

Currently no political party in Parliament has policies or is arguing for policies that would reverse this massive massive wealth bonus for the wealthy due to a Governmental decision. The Greens have only weakly argued this line, but also have no leverage in any coalition forming negotiations because they have pledged always to go with Labour. The Government has ruled out a wealth tax in this term, has ruled out a Capital Gains Tax for all time (or at least while the PM is the PM), and has again recently ruled out an inheritance tax.

Both major party leaders have also said they would not house prices to fall, even from these elevated levels. The shock of the 30% ratcheting up of prices is yet to reverberate through the political economy. But it will. There will be a reckoning, in the same way the shocks from benefit and spending cuts in 1991 almost cost National the 1993 election and led to the creation of MMP.

Other places I’ve written and spoken

Briefly elsewhere in signs o’ the times news

Useful longer reads and listens

Some fun things

Ka kite ano

Bernard

Share this post