TLDR: Inflation not seen since the eve of the creation of our independent, inflation-targeting Reserve Bank in 1990 has unleashed a blame game that has yet to target the central bank. The Opposition is blaming the Government, which is complicit, but it is the Reserve Bank that should be first in the firing line.

Paid subscribers can see more analysis and detail on the historic inflation figures below the paywall fold and hear more in the podcast above.

That includes my argument for a proper independent Australian-style review of the Reserve Bank’s ‘least regrets’ decisions in the heat of the Covid crisis in March 2020, which caused at least a third of the inflation and can be fairly blamed by a whole new generation of young renters being forced to give up their hopes of home ownership, or leave the country.

The Reserve Bank should have a lot more regrets

Regrets, I've had a few

But then again too few to mention

I did what I had to do

I saw it through without exemption - Frank Sinatra singing My Way

When it comes to monetary policy right now, Reserve Bank Governor Adrian Orr and Finance Minister Grant Robertson are doing their own karaoke duet of the ‘Chairman of the Board’s’ signature tune.

At times, Orr has even appeared Edit Piaf-like in his defence of the Reserve Bank’s actions.

Non, rien de rien.

Non, je ne regrette rien

Ni le bien qu'on m'a fait

Ni le mal, tout ça m'est bien égal

Non, rien de rien

Non, je ne regrette rien - Edit Piaf singing ‘Non, je ne regrette rien.’

So are they justified in having few or even no regrets? In my ‘Harry Hindsight’ view: no. And now there must be an accounting for those regrets, and some learning.

So far, the Reserve Bank’s only self-reflection has been to self-justify and run its own regular five-yearly review of its monetary policy mandate. Meanwhile, Robertson’s arguments have been all about deflecting blame overseas. The Opposition has chosen largely to focus its attacks on the easier political target of Labour’s ‘addiction to spending,’ rather than break the habits of political lifetimes and criticise the independent central bank. Neither of those three strategies is credible in the long run, and all three players only need to look to their colleagues in Australia to see that a truly independent and deep review is needed.

As mentioned above, the new Labor Government of Australia is about to launch a bi-partisan and independent review of the Reserve Bank of Australia’s money printing, which did go on for longer than our central bank’s, but has had broadly similar effects on house prices and inflation.

Also as mentioned above (and below), we now have credible and trenchant criticism from establishment figures of the Reserve Bank such as former Reserve Bank chief economist John McDermott (2007-18) and former Reserve Bank Board Chair Arthur Grimes (2003-13), who was instrumental in building our independent inflation-targeting regime in the first place.

There must be a serious, deep and independent review of the Reserve Bank’s actions in 2020 and 2021, if only to win back the trust of the generation of renters (without generous parents) who are now fleeing to Australia to find renewed hope of home ownership and family lives.

So how did we get here?

The Reserve Bank decided in mid-March of 2020 to throw the kitchen sink at the economy to reassure borrowers, home owners and banks that there would not be a depression because of Covid lockdowns. It said at the time it wanted to pursue a ‘least regrets’ policy.

However, within months it was clear the panic was past and the economy was bouncing back into the shopping centres and open homes with a surprising rapidity, along with house prices, jobs and spending. In retrospect, the Reserve Bank should have stopped money printing within a few weeks of the end of the first lockdown in June, or even once the bond markets were unfrozen in May. It should never have removed the LVR controls in April 2020. It should never have started the cheap loans to banks in December 2020, let alone continued expanding them to the present day.

In my view, the Reserve Bank’s mistakes were not made in that momentous week of March 16 to 23 of 2020 as the Government collectively decided on hard lockdowns and the Reserve Bank launched a $30b money printing and bond buying programme, as well as slashing the Official Cash Rate by 75 bps to 0.25%. Least regrets and the kitchen-sink-throwing were appropriate then, in the fog of fears about about 30% unemployment and a global financial collapse. But within a couple of months, the fog was clearing.

Now the regrets equal (some of the) 7.3% inflation

The biggest mistakes were to remove the LVR controls at the end of April and to go on expanding the money printing plans to $100b by August 2020, even though it only used just over half of that capacity in the following year.

Now, after yesterday’s record-high 7.3% inflation data for the June quarter from a year ago, it’s clear the central bank should have at least a few regrets and should be held accountable for them, along with Finance Minister Grant Robertson, who was asked for and gave his approval to the biggest things thrown into that kitchen sink and left there: the money printing; the LVR removal; and the cheap bank lending.

The political blame game over the inflation has so far pussy-footed around the main issue. The money printing, (ongoing) cheap bank loans and LVR removals fired house prices 45% higher by November 2021, and is now being reflected in the demand-driven inflation in building materials, construction costs and rents.

The massive expansion of lending and the sharp rise in house prices was clear by mid-to-late 2020, but it took until June 2021 to explode into the real economy of rising housing costs.

The kitchen sink of monetary policy and prudential policy loosening was done with the clear knowledge of a restrained housing supply and the risk any demand stimulus would have a leveraged effect on house prices, and eventually rents. That is exactly what has happened.

How much of the inflation was domestically generated?

Just over a third of the 7.3% annual inflation reported yesterday can be blamed on that monetary policy loosening. The rest can be sheeted home to higher global food and fuel prices, although that at least partially is due to the massive money printing also done in the United States, Europe, Britain and Australia over the same period. Aotearoa-NZ was not alone in printing money to buy bonds to lower longer term interest rates.

Our Reserve Bank can rightly claim credit for stopping the printing sooner than the rest (July 2021) and starting rate hiking (October 2021) sooner than the rest. Although by then, the Reserve Bank had already printed as much, if not more, in proportionate terms to GDP, than those other central banks, and took the extra step of relaxing LVR controls.

By late 2020 the local genie was out of the bottle

However, within four months, it was clear the worst was over. Instead, the Reserve Bank went on printing and did not properly impose lending controls, stop printing and hike interest rates for another year. That was when the genie got out of the bottle, although it’s still worth saying the domestic demand-driven inflation genie is only responsible for about a third of the inflation.

Even if the Reserve Bank had kept the OCR at 0.25% until October 2021, simply not starting the cheap lending to banks, stopping the printing immediately, and re-installing the LVR controls ,would have reduced much of the damage, especially to house prices and rents, which, for example, are now rising at the fastest rate in history outside of Auckland (5.8%).

It’s time the Reserve Bank and Labour had at least a few regrets and acknowledged them. The Opposition also needs to front up and call for that review, which would at least separate the politicians from the process.

Here’s a more appropriate song for the moment.

I only want one day

One lousy day, that's all

Of every day that's been before

Since time beganI know my prayer's in vain

But for a second, I'll pretend

That I can start today again - Paul Kelly singing ‘If I could start today again.’

What to do now (and not to do)

The temptation for the Reserve Bank now would be to over-react and hike much, much higher than its current plans. Financial markets priced in a rise in the OCR to just over 4.0% yesterday, which is in line with the Reserve Bank’s forecasts from May. If it wanted to do more, it could start by ending and unwinding the $12.7b of cheap loans to banks through its Funding for Lending programme. It could also further tighten LVR settings and unravel its bond-buying programme much faster.

From a fiscal policy point of view, enacting some sort of angry, fast spending crackdown would be counter-productive and too painful for those who can afford it least. If the Opposition were being intellectually honest and wanted to do the least damage, it would propose a windfall profits tax from those businesses who retained the $20b in wage subsidy cash in their savings accounts, and some sort of wealth or land tax to reduce house prices and pressures on rents.

No, I didn’t think so…

Elsewhere in the news overseas and here this morning:

Eliminating GDP - China launched new mass testing of millions in Shanghai and Tianjin overnight as the BA.5 variant establishes itself in our largest trading partner, threatening to extend a sharp economic contraction as President Xi Jinping continues to pursue a Covid elimination strategy. Nomura estimated last night 264m people in 41 cities were locked down and were responsible for nearly 19% of China’s GDP, with vaccination going so slowly that only 80% of over-65s will be vaxxed by July next year at current rates. Reuters

Rationing GDP - Reuters reported this morning Gazprom has told customers in Europe it cannot guarantee gas supplies because of 'extraordinary' circumstances, increasing fears President Vladimir Putin will stop Gazprom from turning the gas back on later this week. The European Union told members to cut gas consumption immediately to rebuild stocks before the winter and avoid heavy rationing for industrial users and home heating. However, even limited gas rationing is expected to cut European GDP by 1.5% of GDP over the next year.

China’s mortgage stress - Chinese authorities moved overnight to censor social media posts about a gathering mortgage boycott by owners of unfinished apartments, while also considering concessions to lenders to complete projects and mortgage holidays for borrowers. Fears are growing the implosion of China’s apartment development sector will add the pressure on growth from Covid lockdowns. Bloomberg, Bloomberg

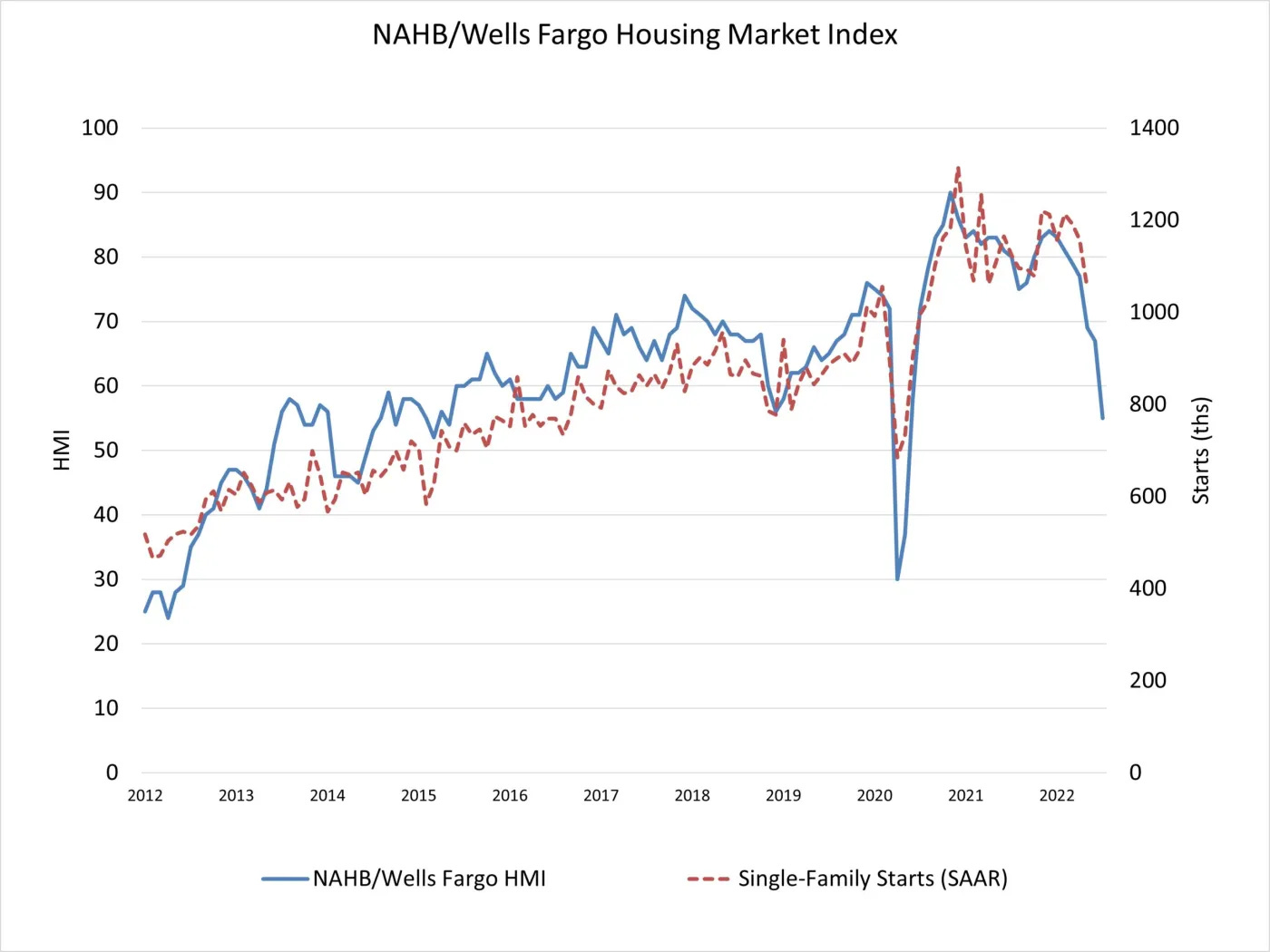

US mortgage stress - In more signs that sharply-higher US interest rates are slowing the world’s largest economy towards recessionary levels, data out overnight showed home builder sentiment slumped in July to its lowest level since the worst of Covid in early 2020 (see more in chart of the day below). The result was much worse than expected, but, ironically, helped drive a rally on US stock markets as hopes grew it would see the US Federal Reserve hike only 75 basis points next Thursday, instead of 100 basis point. Reuters

Grimes blames RBNZ - Former Reserve Bank Chair Arthur Grimes has launched a scathing attack on the bank’s handling of Covid stimulus, which led to a 45% rise in house prices and upwards pressure on rents. Grimes was quoted on the front page of the Dominion Post today by Thomas Manch as saying the Reserve Bank had been incompetent by easing too much before and during Covid, and now needed to cause the economy pain to stop inflation expectations getting out of hand. (See more in quotes of the day below).

Australia’s central bank review - New Labor Treasurer Jim Chalmers said yesterday he wanted a full bi-partisan and independent review of the way the Reserve Bank of Australia handled Covid, with the terms of reference due within days. WAToday

Number of the day

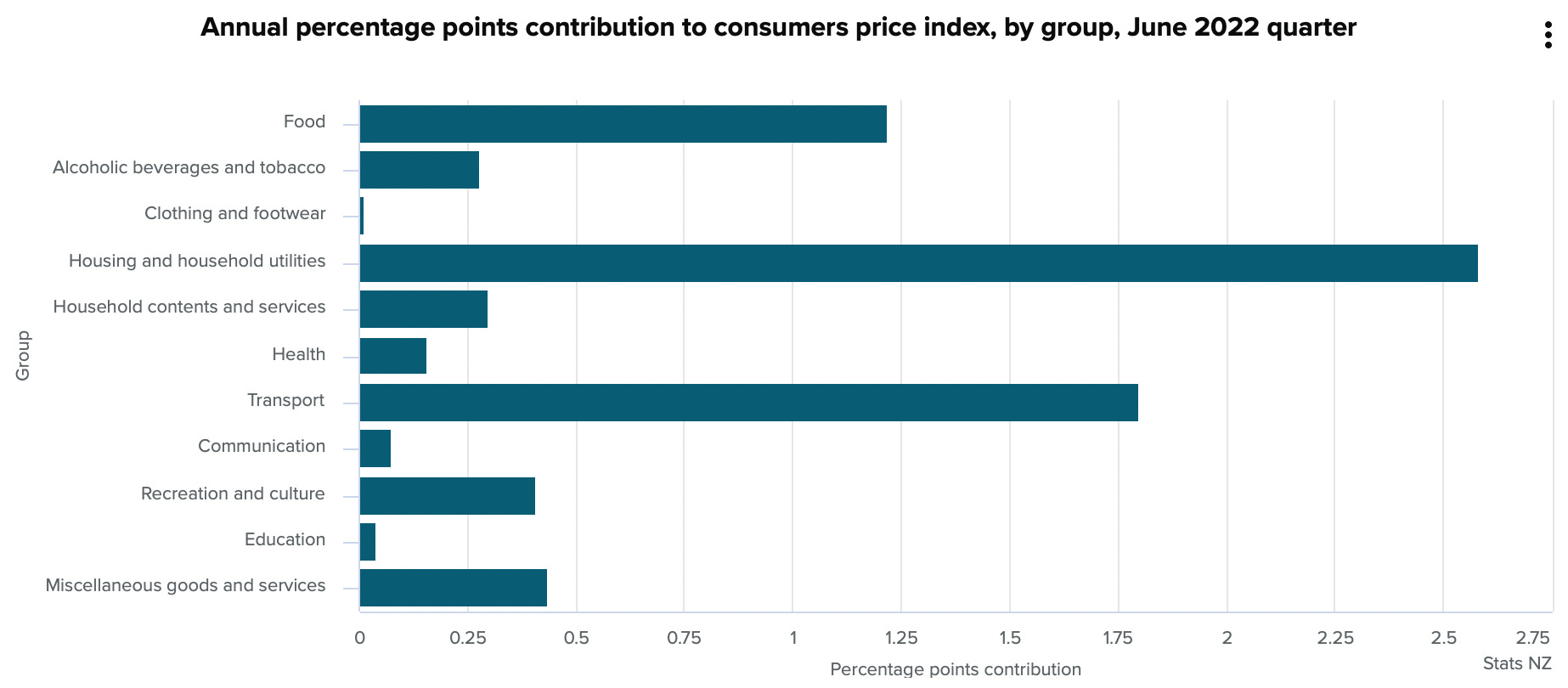

Housing inflation’s contribution to the CPI shock

35.7% - That’s the share of the 7.3% annual inflation that is due to higher rents and higher house-building costs (55.6 basis points of the 170 basis points for the June quarter).

Quotes of the day

Arthur Grimes accuses the Reserve Bank of incompetence

“They're completely to blame for allowing this to happen. They’ve been incompetent, they’ve been really incompetent.

“There’s going to be people who made plans and interest rates are going to be a lot higher than what they budgeted on, and they’ll have to be higher, because of the mistakes the Bank's made, and it’ll catch people unawares: bankruptcies and people losing their houses.

“If we’re getting 7% domestic inflation now, and rents going up, and if wages start going up a lot, then it could become quite entrenched above 3%. And that’s when the Reserve Bank really has to cause more pain to bring it down.” Former Reserve Bank Chair Arthur Grimes as quoted in the Dominion Post by Thomas Manch.

Another leadership challenge for Green Co-Leader James Shaw

“There has been a small group of people who have been wanting to see the back of me ever since they saw the front of me.” James Shaw talking to 1News.

Chart of the day

US builder confidence fell 12 points to 55, vs expectations for 65

Some fun things

Ka kite ano

Bernard

Share this post