TLDR: The five signals I picked out from the noise this week were:

Reserve Bank Governor Adrian Orr’s second term is hanging in the balance as he scrambles to drag inflation down and have some sort of outside review before March;

A call from the Human Rights Commissioner for a rent freeze and an increase in the accommodation supplement exposed again the Government’s lack of a housing affordability target to hold it accountable;

Fresh emissions reductions commitments without funded investment plans from the Auckland and Wellington City Councils exposed again the performative nature and magical thinking behind central and local Government climate pledges;

China eased monetary policy after surprisingly weak factory output and consumer spending figures for July, adding to the recessionary forces building in the global economy that are expected to drag inflation lower later this year.

China increased subsidies for coal-fired power stations to offset lower hydro-power output caused by climate-change-driven droughts, showing how hard it is for even the last democratic emitters to avoid short term-thinking to solve a long term problem.

I co-hosted our weekly live ‘hoon’ webinar for over 100 paying subscribers with Peter Bale at 5pm on Friday night to talk about these events of the week and others with special guest Raf Manji, who is the leader of The Opportunities Party. The audio from the webinar is in the podcast above for all subscribers immediately as part of this weekly summary and sampler of the week’s news and my work this week on The Kaka.

In particular, we talked about

The Reserve Bank’s rate hike and the challenges it faces reassuring politicians and voters that it needs to remain independent;

the threat to local democracy from the slate of Voices For Freedom candidates in this year’s council elections;

the risks of a new Chernobyl-style nuclear catastrophe at the Zaporizhzhia power plant in Ukraine;

TOP’s proposal for a residential land value tax.

A reminder to free subscribers reading here that we have a special $30 a year deal for under 30s and anyone on a benefit. We also have a new special $65 a year deal for over 65s who are renting and reliant on NZ Superannuation. Any students, teachers and staff who signs up to the free tier with a .school.nz or .ac.nz email address will also be comped up to the full paid tier for free.

This week’s five signals from the noise

Adrian Orr refused to say if he wanted a second term

The Reserve Bank hiked the Official Cash Rate by 50 basis points to 3.0% as expected on Wednesday and forecast it would raise it to around 4.0% by the end of the year. That didn’t surprise anyone in financial markets or change fixed mortgage rates.

The hottest questions at the news conference with the quarterly August Monetary Policy Statement were around the criticism of the Reserve Bank’s performance and whether Governor Adrian Orr wanted a second term. His current five-year term expires at the end of March and a second-term would potentially see him having to serve under a Government run by National and ACT, both of whom have been sharply critical of the bank and Orr.

Orr refused to say whether he wanted a second term, even though Finance Minister Grant Robertson has expressed confidence in him and has said he is working with the Reserve Bank board on the details of the reappointment. National has called for an independent inquiry into the bank’s performance before any decision on Orr’s reappointment.

Orr used the news conference to frame an ongoing Reserve Bank-commissioned review of the central bank’s operation of monetary policy as enough of a review. In particular, he pointed to a part of the review being done by independent overseas experts, former Reserve Bank of Australia monetary policy board member (2001-2011) Warwick McKibbin and former Bank of Canada Deputy Governor Larry Schembri (2013-2022). Here’s my fuller report and analysis in Thursday’s Dawn Chorus.

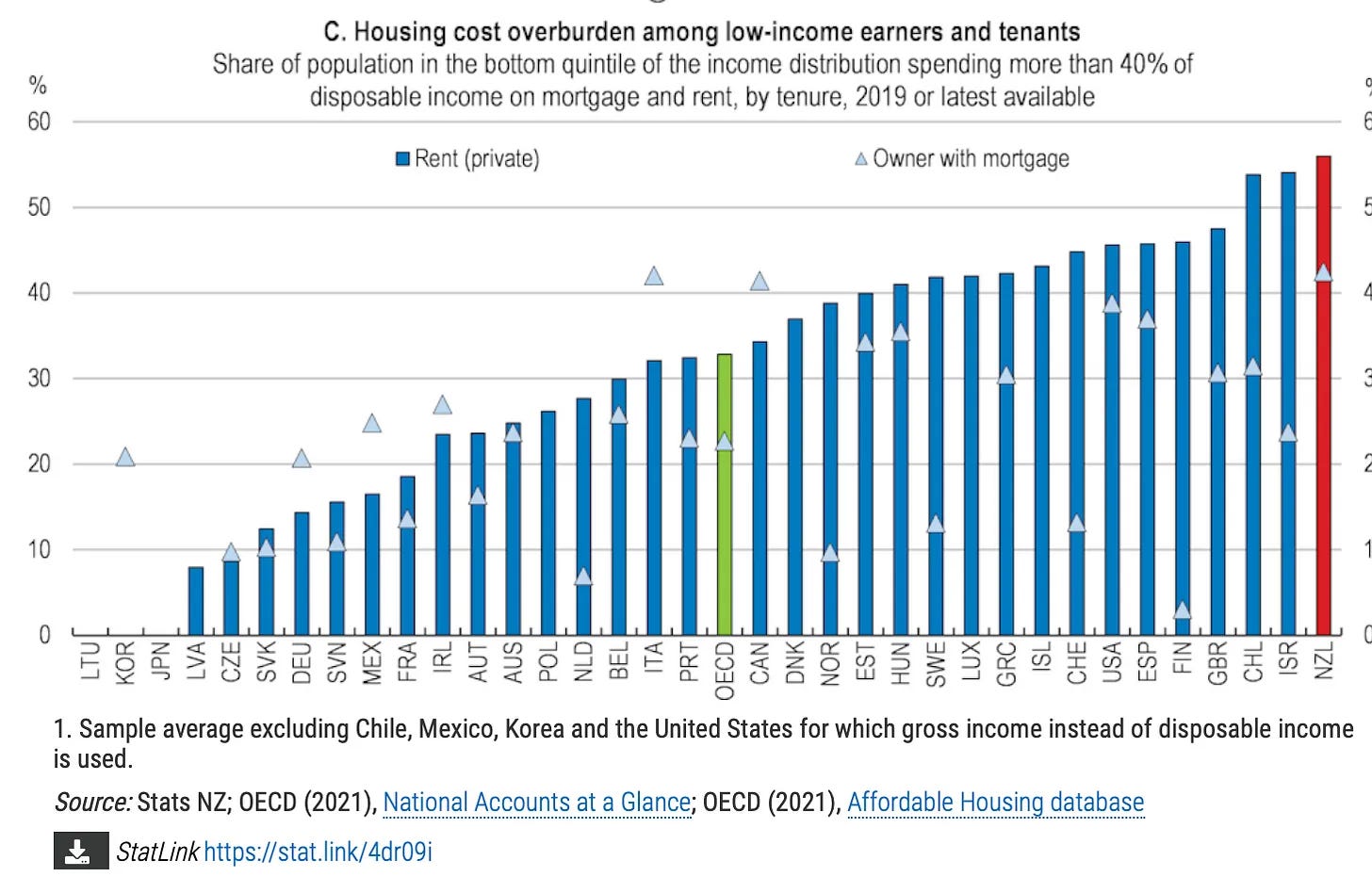

Where’s the affordability target?

Human Rights Commissioner Paul Hunt called this week for a new rent freeze and an increase in the Accommodation Supplement. Housing Minister Megan Woods responded with a list of the Government’s actions to increase housing supply and reduce demand from rental property investors.

I focused in Wednesday’s Dawn Chorus on why the Government’s failure to identify a house-owning and rental affordability target (something like three times income for owning and 30% of disposable income for renting) makes that list a pointless exercise because its impact cannot be measured or the Government held accountable.

Who do they think they’re kidding?

Auckland Council agreed this week to a Transport Emissions Reduction Pathway that reduces climate emissions by 64% by 2030. The plan requires:

a 10-fold increase in walking, cycling and scooter use;

a six-fold increase in bus, ferry and train use;

EVs to be responsible for 32% of total vehicle kilometres travelled by 2030; and,

reductions in freight emissions of 45% by 2030, aviation emissions reductions of 50% by 2030 and shipping emissions reduction of 50% by 2030.

Two things are required to make this work: congestion charging and an awful lot of new central Government funding, neither of which have been agreed. These are easy things for an outgoing Mayor and a bunch of councillors to say with a couple of months left on their term.

China’s economy is slowing fast, which will help reduce inflation

China’s central bank eased monetary policy unexpectedly this week after the world’s second largest economy reported factory production fell and consumer spending growth was weaker than expected because of Covid lockdowns and cooling demand for exports.

Along with easing economic growth in the United States and Europe, China’s slowdown is taking pressure off inflation and encouraging financial markets to think the US Federal Reserve will have to start cutting interest rates next year. The Fed is not saying that though, potentially creating a dangerous gap between market expectations and central bank actions.

China lifts coal subsidies to offset climate-caused cuts in hydro-power

I wrote in Friday’s Dawn Chorus about China’s decision to increase subsidies for coal-fired power plants to help them cope with electricity shortages because of a drought in China’s south-western province of Sichuan.

China is doing what most of the world is doing right now in the face of intense short term financial and climate pain. It is turning to the short-term tools it has to deal with the short-term pain, even though it knows it will make the long-term problem of climate change worse in the long-term. Politicians, even the ones in undemocratic dictatorships, are afraid of the short-term consequences of unhappy voters and citizens having to cope with short-term pain.

Ka kite ano

Bernard