TL;DR: The taxpayer is set to pay banks upwards of $3.3 billion in interest costs on over $53 billion of cash balances they’ve built up in settlement accounts at the Reserve Bank since covid, Jenee Tibshraeny has revealed in a NZ Herald-$$$ scoop this morning from documents obtained under the OIA.

Financial Minister Grant Robertson considered forcing the Reserve Bank (Te Pūtea Matua) to pay banks a lower interest rate than the official cash rate they’re currently being paid. Cutting the interest rate would in effect be a type of bank tax. But the Government has appeared not to proceed with the idea after Treasury and the Reserve Bank said it was worried the banks would in turn reduce their own interest rates on term deposits, which would frustrate its efforts to encourage consumers to save more with banks and thus reduce inflationary pressure.

I include more detail and analysis in the podcast above and below the paywall for paying subscribers

Why ‘hard-working kiwi taxpayers’ pay banks billions

Cheap loans and expensive cash accounts - So it turns out the taxpayer is not only subsidising already-very-profitable private banks with $19 billion of cheap ‘Funding For Lending’ loans that helped pumped up house prices in 2021, but taxpayers are also paying the banks upwards of $2 billion a year in interest for cash banks have to keep with the Reserve Bank. Most regular savers aren’t paid interest on cash accounts with these banks, but the Reserve Bank is paying.

Meanwhile, the Government is skimping on wage settlements for teachers and nurses, delaying infrastructure projects, restricting drug funding and refusing demands from child poverty activists for incomes for beneficiaries and poor families that even the Social Development Minister Carmel Sepuloni acknowledged yesterday (via Q+A) did not allow poor people to live in dignity.

How can the Government argue with a straight face from now on that it has no choice but to cut funding for transport, health, education, climate change, benefits and infrastructure, when it is providing billions in subsidies for bankers and effectively transferring wealth from savers and renters to home owners.

It’s all about the QE in 2020 and 2021

This is a direct result of the $55 billion worth of Quantitative Easing or money printing that the Reserve Bank did in 2020 and 2021 to stimulate the economy during covid. The bank created the $55 billion to buy Government bonds from banks and pension funds in secondary markets. That cash was then deposited by banks back in settlement accounts with the Reserve Bank in a type of merry-go-round. The Reserve Bank then pay banks interest on the balances of those accounts at the Official Cash Rate. Reserve Bank data shows those settlement accounts now have over $53.97 billion in them and the Reserve Bank is paying the OCR now of 4.75%, meaning the interest costs are now running at over $2.56 billion per year.

Documents from the Reserve Bank released to NZ Herald-$$$ reporter Jenee Tibshraeny under the OIA show the Reserve Bank is expected to have to pay $3.3 billion in interest on these balances by 2027. Those documents also show the Government looked at cutting the interest rate to zero, as suggested by former Bank of England Deputy Governor Paul Tucker in a paper into the issue in October last year.

Finance Minister Grant Robertson then sought advice on whether the cash settlement rate could be cut here as an effective form of bank tax. The Reserve Bank advised against it, saying it might lead to the banks cutting term deposits for private savers, which might encourage more of them to spend and add to inflationary pressures. It was also concerned the move would suggest the Reserve Bank was too cosy with the Government.

Here’s more detail in Jenee’s article, which is a follow-up to one she did in October last year (NZ Herald-$$$):

Documents released to the Herald under the Official Information Act (OIA), show Robertson explored whether the RBNZ could save the Crown money by paying banks less interest on the settlement cash they keep at the RBNZ.

The RBNZ currently pays banks interest at the official cash rate (OCR) on their deposits at the central bank, used to settle transactions with each other, the RBNZ and the Crown.

The issue, from a public finance perspective, is that programmes the RBNZ used to lower interest rates in 2020 and 2021 – the Large-Scale Asset Purchase programme and Funding for Lending Programme – saw the balances of banks’ settlement accounts rise seven-fold to $49 billion. (This was by the time of the advice. They were $53.97 billion by the end of January)

These balances are expected to fall as the programmes are unwound. But in the meantime, the RBNZ is paying increasing rates of interest (the OCR is 4.75 per cent and expected to rise further) on a large sum of money.

‘We don’t want the banks to then pay their savers less’

Jenee then quotes from advice provided by Reserve Bank Deputy Governor Christian Hawkesby, who in November NZ Herald-$$$ he opposed the concept, fearing it could hamper the transmission of monetary policy.

He worried paying banks less interest while trying to get them to lift their mortgage and deposit rates could complicate things.

He said the RBNZ’s priority was to lower inflation in line with its mandate, and if the aim of paying banks less interest was to effectively tax them more to help pay for the Covid response, then that was a matter for the Government to consider.

Jenee reports the Treasury briefed Robertson on the issue in November.

It estimated that paying banks no interest on half their settlement balances could save the Crown $3.3b by 2027. But it said that if the Government wanted to tax banks more, it should consider doing so using a different approach.

Changing the rate of interest paid on banks’ settlement balances would produce a volatile revenue stream that would vary depending on the OCR and the size of banks’ balances.

The Treasury also noted the impact the change could have on the implementation of monetary policy and said it could affect perceptions around the RBNZ’s independence.

It suggested Robertson seek advice from the RBNZ if he wanted to further explore the matter. So, he took the issue to the RBNZ, which reported back to him in February.

The Reserve Bank again said it opposed the idea.

It feared paying banks less interest on part of their settlement accounts could prompt them to lower interest rates at a time the RBNZ wants them to keep rates elevated to dampen inflation. It noted paying banks interest at the OCR “creates a floor under short-term market interest rates”.

The RBNZ recognised that both it and other central banks have in the past paid banks different rates on parts of their settlement balances.

But because, in the current environment, this wouldn’t help the RBNZ meet its inflation target or make the financial system more stable, changing the system would be counterproductive and make it look like the RBNZ was too cosy with the Government.

“It would be unprecedented internationally for an advanced economy central bank to introduce tiers for reasons unrelated to their own objectives,” the RBNZ said.

“This policy would amount to a tax on a specific section of the financial sector, which RBNZ lacks public legitimacy to make decisions around and would be in tension with RBNZ’s other objectives.”

Jenee then quoted a spokesperson for Robertson saying: “The minister has not requested further advice on introducing a tiering system at this time”.

Bank tax? Or just no subsidies?

In my view, this is a no brainer. The Government needs to recover something from the banks to offset the billions being paid via the Reserve Bank in effective subsidies via cheap loans and expensive cash settlement account interest costs. The simplest and easiest way is for the Reserve Bank to not pay interest on settlement account balances. Then it should unwind the Funding For Lending Programme loans as quickly as legally possible.

Yes, it may see the banks lower their term deposit rates on savers and force the Reserve Bank to have a higher-OCR-than-would-otherwise-be-the-case to control inflation. That would probably mean slightly higher interest rates for mortgage rates than would otherwise be the case. This makes clearer what is going on here: term depositors without homes and non-home-owning taxpayers (ie renting workers) are subsidising mortgages for home owners and investors, and the profits of bank shareholders in Australia.

How can the Government argue with a straight face from now on that it has no choice but to cut funding for transport, health, education, climate change, benefits and infrastructure, when it is providing billions in subsidies for bankers and effectively transferring wealth from savers and renters to home owners.

It would also be nice to see National and ACT come out against corporate welfare and the use of ‘hard working taxpayers’ money in a way that shifts wealth from renters and savers to homeowners and bank shareholders. Would National and ACT protest if billions of taxpayers dollars were seen to be unfairly going to iwi or beneficiaries or ‘wasteful bureaucrats and consultants’?

When lobbying is unregulated and doors revolve fast

Unregulated lobbyists - Guyon Espiner extended his series of investigative reports on RNZ on Saturday into how lobbyists do their thing in Aotearoa. It is enlightening on the issue of how pine forests are still in the ETS, despite attempts to lever them out. Neale Jones and his work for NZ Carbon Farming (NZCF) is the subject in this one.

In the end, NZCF, which didn't respond to a request for an interview, got what they wanted. The government did a U-turn on its initial proposal and exotics, such as pine, will remain in the ETS.

The government now says a "redesigned" category for exotics could come into effect in January 2025. Guyon Espiner via RNZ

He makes the great point that Aotearoa is an outlier without regulation for lobbyists and no rules on revolving door hiring of bureaucrats, politicians and political operatives alike.

Out of 41 countries analysed, New Zealand was one of nine to have no law restricting movement between top government jobs and the lobbying industry.

In Australia departing ministers cannot "engage in lobbying activities relating to any matter that they had official dealings with in their last 18 months in office".

Heads of government agencies, senior public servants, ministerial staff and even defence force staff (at colonel level or above) face a 12 month cool off period before they can join lobbying firms.

Canada has a five year stand down period; Spain two years and Germany 18 months.

In New Zealand, cabinet ministers can go straight into lobbying jobs, taking knowledge, information and contacts to be leveraged in the commercial sector. Guyon Espiner via RNZ

Lobbyists should be regulated and the revolving door dismantled

Again, this is a glaringly obvious thing that should be done to maintain public confidence in Government. Labour politicians like to talk about social license, but when it’s clear this month’s ‘policy bonfire’ included a bunch of policies on alcohol harm, recycling and climate change that lobbyists effectively blocked, then there is a problem.

Is it any wonder the status quo is so powerful under MMP and there is little real action to deal with climate change, housing affordability and poverty? The interests that benefit from slow-to-no-policy-change have paid for close and fast access to those trying to change policies.

Here’s the best (and only) source of organised information on who is a lobbyist in Aotearoa. It is Parliament’s approved visitor list for Parliament, which is a list of lobbyists given swipe cards by operatives.

Other scoops and notables this morning

Just imagine if it was free? Demand for dental work has skyrocketed since the Government rose the grant cap from $300 to $1000 for people on low incomes and benefits, with nearly $15 million paid out in three months, Michael Neilson reported for NZ Herald this morning.

Useful reports and research

Housing quality, cost and precarity in Queenstown - Here’s the latest Queenstown Lakes District Council annual quality of life survey results, which show 5% of the population have used emergency accommodation in the last year, 16% don’t have a steady place to live, 26% either couldn’t afford to heat their home at all or not much, and 20% were forced to move by: an expiring lease, the landlord was selling the home, the home was mouldy and/or cold, they bought a home or their home was being turned into a rental. It came out on Friday.

This quote from a respondent to the survey stood out for me:

“We are about to have our first child and have had to move at least every 12 months due to either affordability, unhealthy home, and recently away from shared housing. We are genuinely concerned about our end of lease date in March 2023 and whether we can find a healthy, affordable home for us and our new born baby within the district. It also makes it difficult to plan for enrolling in child care as we don’t know where we may be living year to year. We would like to purchase our own home for long term living but as all properties available for sale are up for auction we are unable to adequately put aside a set budget.” Queenstown Lakes District Council annual quality of life survey results

The Housing and Urban Development Ministry (HUD) released a report last week: Evaluation of whānau experiences in contracted emergency housing in Rotorua. The report generally says the use of motels is positive, but not a long-term solution. This quote stood out for me:

Housing is both a cause of detrimental health, education and social outcomes and also a solution and catalyst to wellbeing. HUD report: Evaluation of whānau experiences in contracted emergency housing in Rotorua

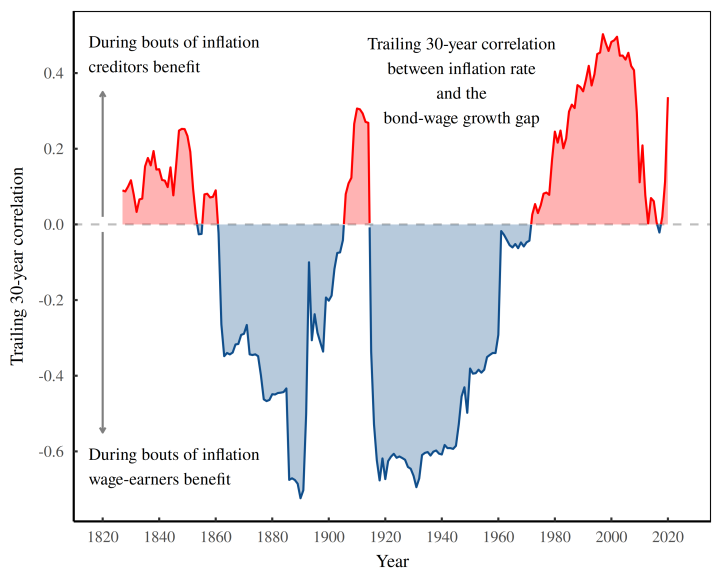

Chart of the day

Who benefits from inflation over time in the United States

Blair Fix has written a fascinating paper on the winners and losers over time from inflation, and how the battle and arguments over inflation is as much a political struggle over the shares of income as it is an economic one.

Profundities, spookies, curiosities and feel goods

Cartoon of the day

Ka kite ano

Bernard

PS: Do you want me to open this up? Please note that I would have to remove the paywalled quotes from Jenee’s story first.

Share this post