Why lifting interest rates now was a bad idea

RBNZ hikes OCR by 25bps to 0.5% and sees more hikes to come, despite noting acute stress in Auckland and services sector businesses and a cooling of global and Chinese growth outlooks

TLDR: The Reserve Bank has just increased the Official Cash Rate by 0.25% to 0.5%, its first hike in seven years and in line with financial market and bank economist expectations.

It said it expected to keep increasing interest rates over the next year or two towards more neutral levels, which are seen closer to 1.5-2.0%. That would lift mortgage rates back over 5%. The NZ dollar rose about a quarter of a USc to 69.8 USc.

But in my view, starting this tightening cycle now will be seen as just as premature and misguided as the last two failed attempts to ‘normalise’ rates over the last 13 years since the Global Financial Crisis. It is hiking when the largest chunk of the economy is stressed and in a severe lockdown for many weeks to come, and at a potentially very volatile time on global financial markets and for our largest trading partner. Waiting another six weeks to see how the only-days-old abandonment of the Covid elimination strategy would play out would not have restricted the bank’s options too much. There is still too much doubt over inflation generally, and wage inflation in particular.

Instead, it has started tightening much earlier than its near peers, the Reserve Bank of Australia, the European Central Bank and the US Federal Reserve, and without proof that the potentially transitory effects of a global supply shock and volatile demand are turning into some sort of more permanent inflationary threat. Other central banks are still waiting to see the whites of the eyes of inflation, and wage inflation in particular, before acting to tighten conditions.

We’ve been here before

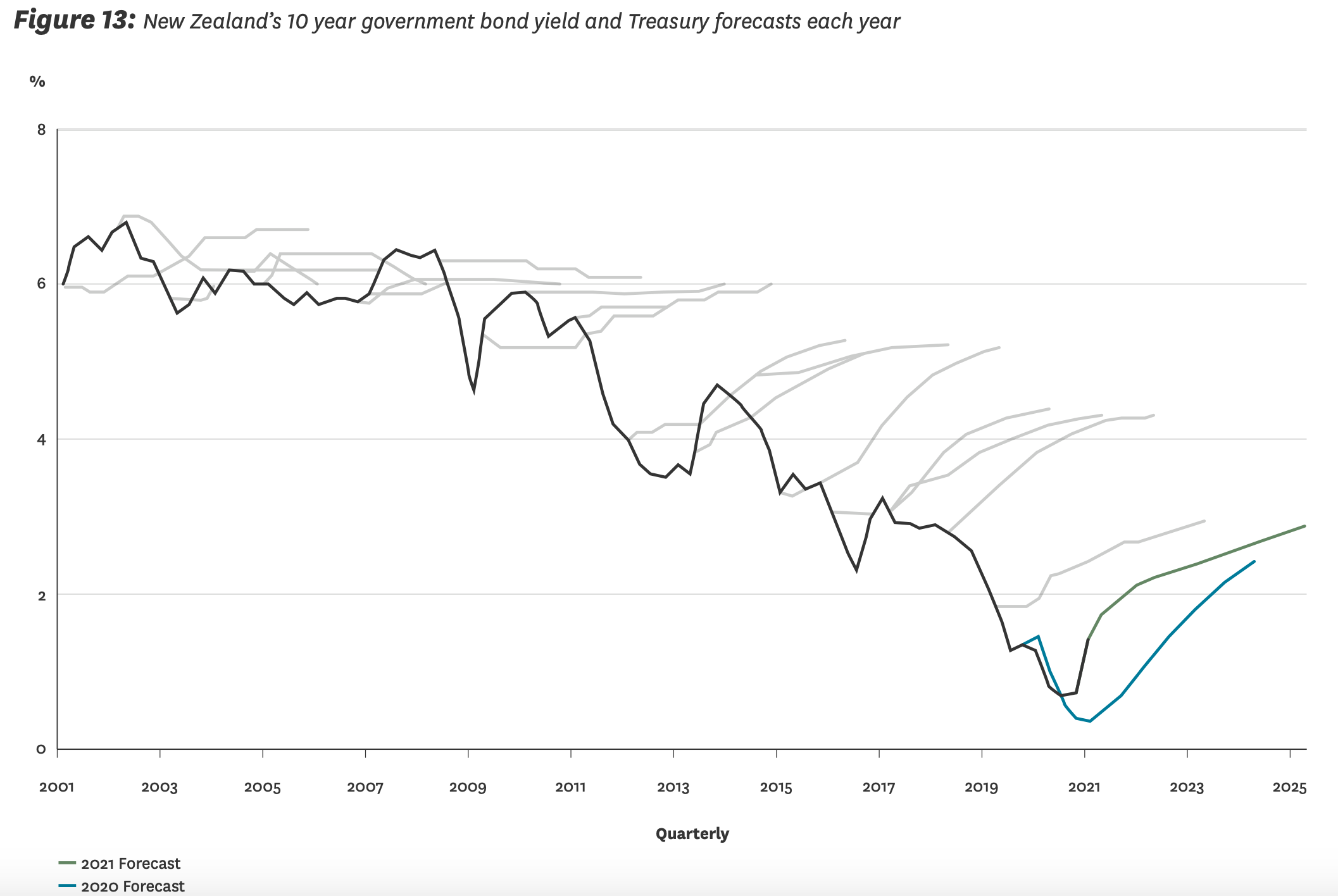

The Reserve Bank hiked the OCR 50 basis points to 2.5% in mid-2010, but had to reverse that within nine months, partly because of the Christchurch earthquake, and partly because inflation was weaker than it forecast. It made a similar mistake in 2014 when it lifted the cash rate by 100 basis points to 3.5%. It had to reverse that hike within a year and then keep cutting it to 1.0% over the following three years.

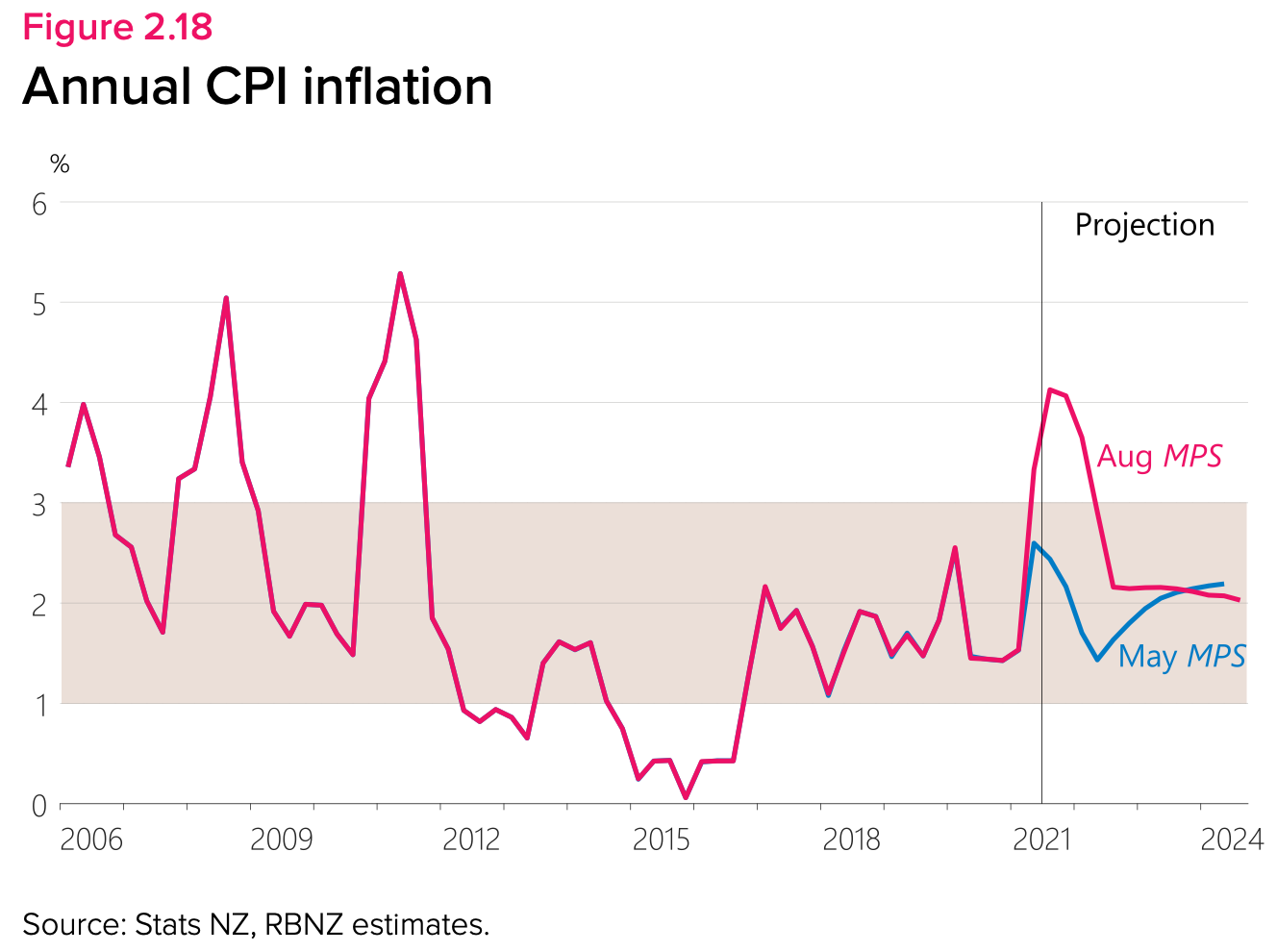

Over the last decade inflation has been consistently in the bottom half of the 1-3% target band and consistently lower than the Reserve Bank’s forecasts, Treasury’s forecasts and the rest of the bank economists’ forecasts for both inflation and interest rates.

Where was the self reflection on past failings?

The Reserve Bank has never done a formal review or acknowledged these forecasting failures and the premature hikes that followed them. Those failures have meant inflation was lower than the middle of the target band, and therefore employment was lower than would have been the case if the Reserve Bank had correctly forecast inflation and the economy’s spare capacity.

Yet it is pushing ahead again with rate hikes, even though its own forecasts show underlying inflation barely above the middle of the 1-3% band in the forecast period, let alone above the 3% top of the band.

For all but a couple of quarters in the last decade, annual CPI inflation has been consistently below 2% and below 1% for a combined two years in that period. This raises the question of whether the Reserve Bank is being asymmetric in its use of monetary policy - ie does it react harder and earlier to rising inflation than falling inflation.

It should treat the risks symmetrically and there’s a case it should use the approaches adopted in the last two years by the US Federal Reserve and the European Central Bank of allowing inflation to run hotter than the middle of their target ranges to offset the decade of under-inflation. Effectively, they have adopted average inflation targeting over a longer period. It’s partly the reason why they are nowhere near putting up interest rates in the next year.

Those central banks acknowledged their forecasting and policy failures over the last decade and are acting now to offset them. Both still have their official cash rates near zero and are printing US$120b and €80b per month to buy Government bonds to lower longer term interest rates as well.

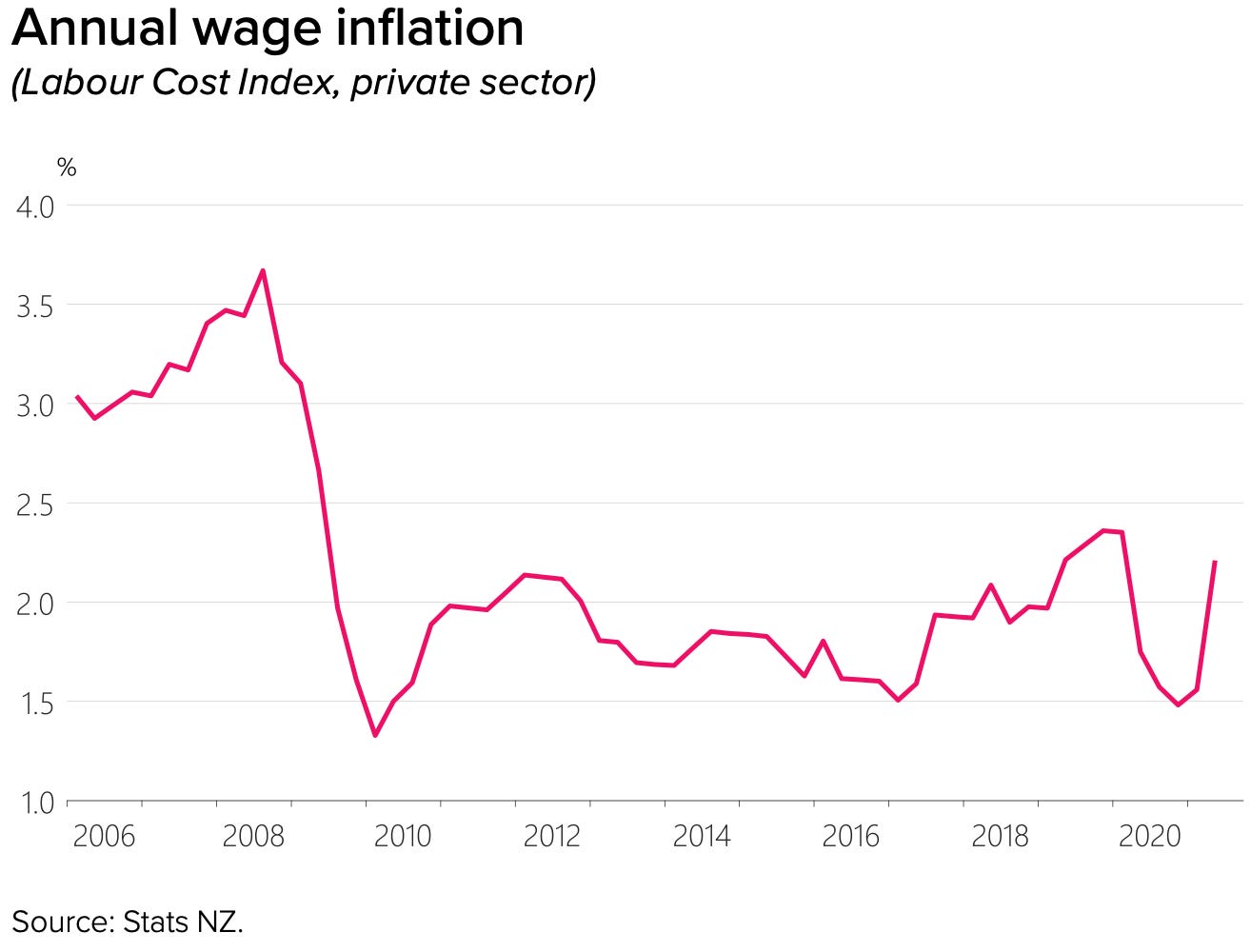

Also, the Reserve Bank is out of line with the Reserve Bank of Australia which has pledged not to hike until early 2024 and not until wage inflation rises from its current 1.7% to over 3%. New Zealand’s wage inflation was just 2.1% in the June quarter, despite all the talk of labour shortages and has been structurally lower for more than a decade.

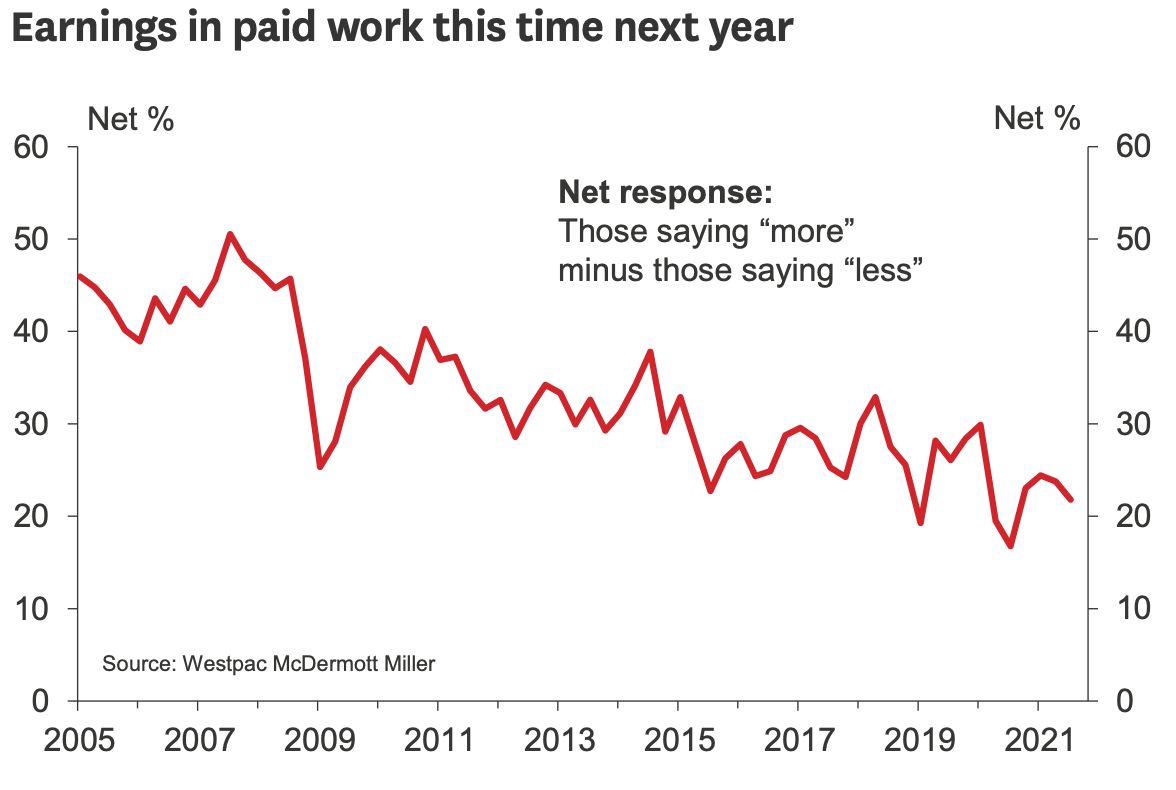

Business opinion surveys have shown significant stress over labour shortages this year, but they have yet to turn into significant wage inflation. Workers themselves do not expect significant wage hikes. The Reserve Bank focuses a lot of business expectations of inflation, but less so on worker expectations.

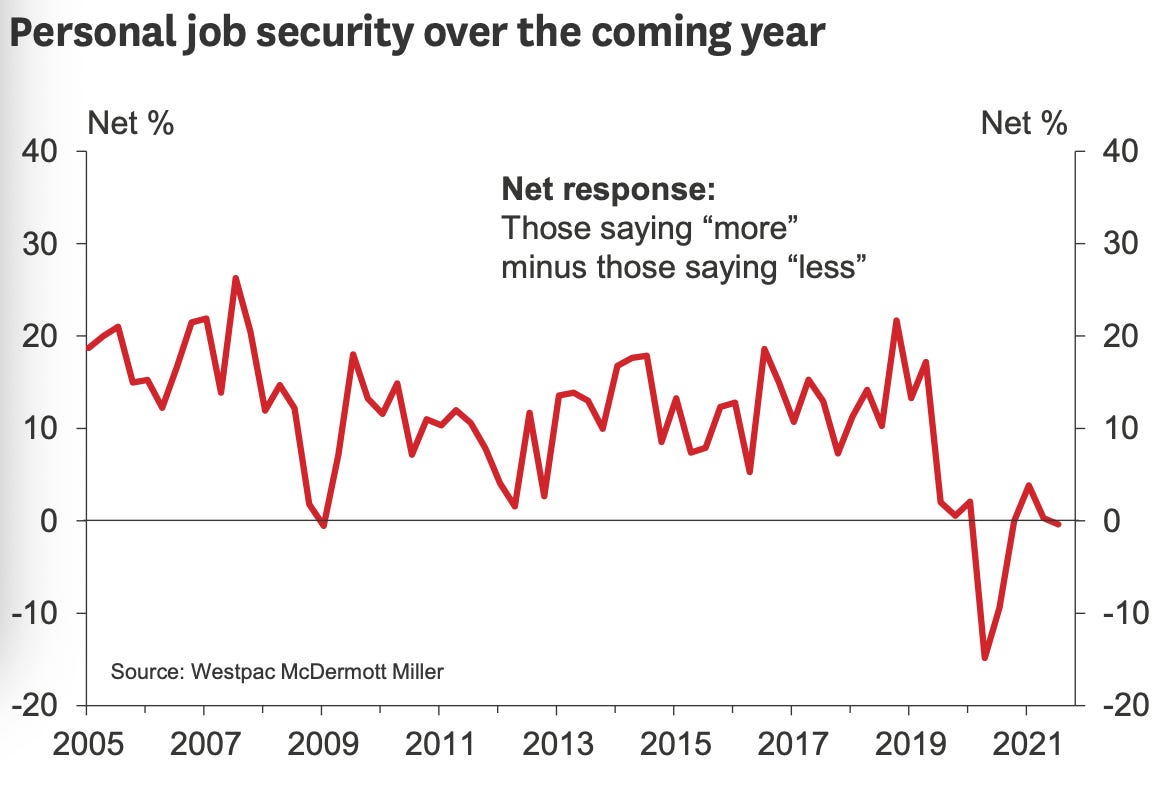

The McDermott Miller Westpac survey of employment confidence for the September quarter found another fall in the portion of workers expecting higher earnings in the year ahead, while perceptions about job security continue to fall.

So what changed since August to warrant the hike?

The Reserve Bank said itself with its full Monetary Policy Statement on August 18 it had been ready to start the hiking cycle, but held off because the nation had been thrown into level four restrictions the previous day.

So a steady-state economy from then would, in theory, justify going ahead with the rate hike today. So what has happened in both our economy and the global economy since August 18?

Our lockdowns have dragged on longer than expected since then and look set to continue up until Christmas in only barely looser terms in Auckland, and still in restricted form in the rest of the country. Most economists now expect a significant contraction in September quarter GDP with a slower rebound in the December quarter than was seen after the end of lockdowns last year.

Since August 18, small businesses in Auckland, especially in hospitality and events, have been hit hard. The rest of the country’s tourism and hospitality businesses are also struggling under the longer and heavier restrictions for longer. If anything, the domestic news since August 18 has been worse than expected, and even more so this week as the Covid restrictions have widened and have less prospect of being removed in the coming weeks.

China weakens and US default beckons

It’s also been worse than expected overseas because of continued supply chain disruptions and the extended effects of delta outbreaks. The IMF last night cut its global growth forecast and warned of the potential for significant financial market volatility in the months ahead. China’s factory production contracted surprisingly in August and its largest property development company has stopped work and is dealing with a cash crisis.

There is also the very-real risk of a default by the US Government in the crucial market for US Treasuries in mid-October. Treasury Secretary (and former US Federal Reserve Chair) Janet Yellen has warned the bedrock of the global financial system could fracture from October 16 if the US Congress does not increase the Government’s debt ceiling.

So what was the Reserve Bank’s justification?

The Reserve Bank statement today (it is an ‘in-between’ decision without a full set of fresh forecasts and a news conference) actually acknowledged the increased uncertainty since mid August, the extra stress for Auckland services sector businesses, and the cooler growth prospects overseas.

But it pointed instead to “cost pressures becoming more persistent and some central banks have started the process of reducing monetary policy stimulus.”

The only other developed country central bank to hike this year is Norges Bank in Norway, where record oil and gas revenues have fueled inflation. Our closest peers are at least a year away from tightening.

The Reserve Bank’s statement today made no reference to the abandonment of the elimination strategy, or the rise in the recent week of cases, or the widening of alert level three restrictions to the Waikato. Over two million of New Zealand’s five million people are now in level three restrictions, which are currently tougher than either the UK, Australia or the United States.

The Reserve Bank did point to other positive factors.

“While the economy contracted sharply during the recent nationwide health-related lockdown, household and business balance sheet strength, ongoing fiscal policy support, and a strong terms of trade provide confidence that economic activity will recover quickly as alert level restrictions ease. Recent economic indicators support this picture.” Reserve Bank statement with rate hike.

However, fiscal support this time has been much less than last year. Just over $14b was paid in cash to businesses last year. So far this year, it has been around $3b.

The Reserve Bank is also worried about supply shock inflation spreading.

“These immediate relative price shocks risk leading to more generalised price rises. At this time, measures of core inflation and medium-term inflation expectations remain close to 2 percent. The Committee noted that further removal of monetary policy stimulus is expected over time, with future moves contingent on the medium-term outlook for inflation and employment.” Reserve Bank

But so far there is little evidence of widespread inflation setting in, or inflation expectations spiralling out of control.

The Reserve Bank has pulled the trigger upon seeing the cloud of dust on the horizon, as it has done for thirty years on the presumption inflation is a sleeping dragon that must always be slain from a long distance. That was the wrong approach for the last decade. It should have waited it could see the whites of the eyes of inflation, or at least until we are sure Auckland’s restrictions are lifting and our delta outbreak is contained.

Let’s hope it is not a repeat of the 2010 and 2014 premature rate hikes, when the bank chose ‘Ready, fire, aim’, rather than to be sure of widespread inflationary pressures and then fire off the rate hikes.

I’d say the amount of debauchery & financial market madness since the global ‘COVID related’ monetary authorities went cray, is well past it’s due date to end. I’m not sure you can advocate zirp, qe, minting T$ coins, mmt, AND call for lower asset prices. They go hand in hand. In a year when already historically well overvalued assets performed as they did, you can’t hide behind ‘mandate targets’. Societal impacts of inequality enhancing policies are rampant and obvious everywhere. This trend has been ongoing since ‘qe’ became the norm rather than the exception, & of course won’t be addressed until we get a 2008 repeat. They’ve extended the cycle, but damn it’s quite a disturbing world they have created in many ways.

An attrocious decision, but what do you expect. NZ was amongst the first nations to implement reserve bank independence and inflation targeting by monetary policy, and the entire civil service is now ideologically locked into these paradigms. RBNZ has already stuck up its middle finger at the Finance Minister, who doesnt have the cojones to make the necessary changes, not withstanding his dire need to "protect the surplus". With only one lever to pull they have to pull it or become irrelevant.