TLDR: In this week’s ‘hoon’ webinar in podcast form above, Peter Bale and myself invited on ANZ Chief Economist Sharon Zollner and talked about:

Europe’s energy crisis and how Governments were intervening in markets to impose windfall taxes and pay hundreds of billions in energy subsidies to households;

the European Central Bank’s biggest rate hike in 24 years and why this meant Peter would finally get some interest on his euro deposits;

what the election of Liz Truss means for Britain’s debt and taxes;

Sharon’s view house prices may not fall as much as previously thought; and,

Emmanuel Macron’s speech about the ‘end of the age of abundance’.

We also briefly talked about the Queen’s passing, including Peter’s recollections from meeting her a couple of times. The podcast above is available for all paying and free subscribers as part of this weekly sampler email. Subscribe in full to support my public interest journalism on housing affordability, climate change and child poverty and to join our community debating these issues daily.

My Five Things to note this week

Our housing crisis writ large in Rotorua

TVNZ’s Sunday programme (below) aired a startling documentary exposing bullying of homeless people in Rotorua motels by a charity with unlicensed security guards with gang connections. Opposition parties called for an inquiry. The Government said it hadn’t found anything untoward.

The exposure of the ‘Golden Mile’ highlights again the failure of 30 years of infrastructure under-investment allied with a structural taxation bias in favour of residential property. The Government, like the last one, is now scrambling with short term solutions, but won’t address the core issue:

our taxes and infrastructure investment rates are too low;

we don’t tax capital gains or wealth, unlike every other developed country; and,

there is no immediate political prospect to break this log jam, largely because home-owning median voters like it just the way it is, until they see the end results of child poverty, social dysfunction and rising welfare costs in their faces every day.

The immediate solution is to push the social problems ‘somewhere else.’ That somewhere else in the middle of the North Island is Rotorua. The same ‘Golden Miles’ are in place in many provincial cities up and down the country.

Here’s my weekly ‘When the Facts Changes’ podcast via The Spinoff talking about the housing supply issues with Kiwibank economist Jeremy Couchman, and the Golden Mile documentary below that.

Europe intervenes massively in energy markets

Faced with Vladimir Putin’s act of economic warfare of cutting off their gas supplies completely, European governments are intervening massively in markets to impose price caps and redistribute profits and resources from asset owners to households, or to simply park the cost as public debt and let the owners reap the rewards from more taxpayer-funded bailouts.

European Union countries this week announced plans to imposing windfall taxes on the winners from exploding wholesale gas and electricity prices in order to pay over €500b euros in subsidies to households so they can afford to pay their gas and power bills this winter.

Britain’s new PM Liz Truss announced plans to borrow over £150b to freeze household energy bills. She also announced Britain would start fracking for gas and remove its energy levies designed to reduce climate emissions. She is effectively paying taxpayers’ money to fund profits and cash returns for the energy companies on the right side of the price spikes, and to rescue those on the wrong side.

Europe is now re-organising parts of its economy for a long war, which means pivoting production for war aims and imposing the sorts of rationing and price caps used in war. The video below that emerged this week of French President Emmanuel Macron’s first call with former comedic actor and now Ukraine President Volodymyr Zelensky on the first night of the war is remarkable. It introduces the phrase ‘total war’ to the conversation.

Europe scrambling to contain inflation headed for 10%

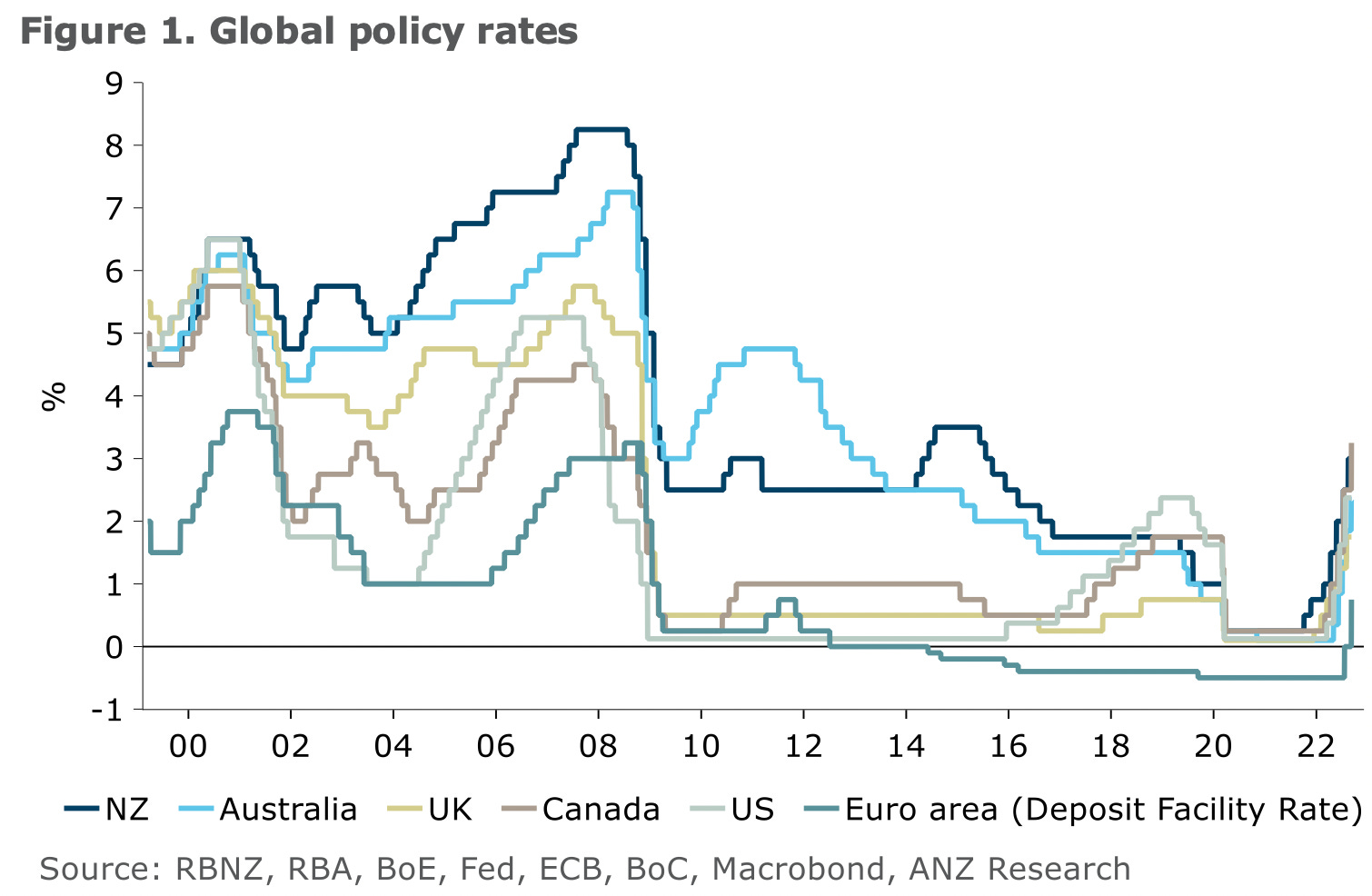

The European Central Bank hiked its main interest rates by the most in the 24 year history of the euro this week. It is battling inflation that is headed for 10% across the continent and faces the prospect of a recession later this year at the same time as double-digit inflation.

Europe’s other problem is it hasn’t yet matched its single monetary policy and currency with a single Government or fiscal policy. It means the ECB has ended up printing money to buy Greek, Italian and Spanish bonds to contain their interest rates, which would normally be much higher because their Governments have higher debts than the rest of Europe. Rising interest rates and the stresses of the winter will put this fundamental weak point in the global economy under enormous financial and political pressure in the months to come.

Vladimir Putin may be losing on the battlefields of Ukraine, but his acts of economic warfare on Ukraine’s immediate suppliers of support and arms is having an extraordinary effect. As Peter points out in the podcast above, Italy’s leaders are now openly talking about trying to negotiate with Putin to resume gas supplies.

We talk about Europe’s economic and political woes with Sharon in the podcast above, as well as whether the US Federal Reserve will win its battle of wills with markets. The Fed reiterated again this week it is very determined to squeeze the US economy with rate hikes until the pips squeak to beat down inflation, while markets see inflation solving itself and the Fed eventually relenting so asset prices can stay high.

Underlying all these problems is the very live issue of whether central banks can maintain their independence in the face of political pressure to solve Government debt and economic growth problems by just inflating away the debt.

‘The end of the age of abundance’

On August 24, Macron gave a sobering short speech to his first post-summer cabinet meeting on what faced them. In the process, he became the first world leader to openly talk about ‘de-growth.’ This is the idea that the planet is hitting its physical limits and the task now is to manage a decline in GDP and a redistribution of resources to stop the earth from cooking and dissolving into a Mad Max-style hellscape of wars over energy and water.

Here’s what he said:

“What we are currently living through is a kind of major tipping point or a great upheaval … we are living the end of what could have seemed an era of abundance … the end of the abundance of products of technologies that seemed always available … the end of the abundance of land and materials including water.

“This overview that I’m giving, the end of abundance, the end of insouciance, the end of assumptions – it’s ultimately a tipping point that we are going through that can lead our citizens to feel a lot of anxiety. Faced with this, we have a duty, duties, the first of which is to speak frankly and clearly without doom-mongering.” Emmanuel Macron talking to his cabinet. Guardian

I wrote a piece on Wednesday about how 30 years of magical thinking had led us to this point. Here’s the guts of it.

This magical thinking says voters in a property-owners’ democracy can have:

low taxes, low debt, low interest rates and rising asset prices into infinity;

without having to invest much in repairing or preventing the damage to the environment, or in new technology to use energy more efficiently;

or having to invest in affordable housing or transport for the generations of youth sentenced to live as renters on precarious wages for decades to come;

or don’t have to worry about election revolts from those unborn generations who will have to pay both rent and taxes for the publicly-funded pension and healthcare costs for today’s asset owners;

that democracies can easily survive the social stresses and lower economic growth rates caused by widening inequality, over-consumption of physical assets without paying for externalities, and unaddressed climate change; and,

that autocracies competing for those resources with democracies will not take advantage of this dysfunction to protect and grow their own share of those resources.

The bottom bottom line - None of this really computes in the long run and it’s beginning not to compute in the short run either as climate change accelerates into growth-sapping events in the near-to-now future.

For example, just overnight:

offices closed and data centres were flooded in the global outsourcing capital of Bangalore after record-setting torrential rains allied with poor water infrastructure investment; (ABC)

California, the world’s fifth biggest economy, is in severe drought and faces power blackouts and water shortages because of climate change Reuters;

a third of Pakistan, which is being bailed out by the IMF, is under water and it’s trying to widen a breach in its biggest lake to avoid it overflowing even more Reuters; and,

Shenzen, the globalised supply chain’s component assembly centre, is locked down with a disease (Covid) initially transmitted zoonotically on a planet that transmits more diseases zoonotically as it warms Reuters.

The unpriced-and-unpaid-for externalities generated by over-consumption, under-investment and deliberately widening inequality over the last 30 years appear to be coming together in a poly-crisis moment. The bill feels as if it’s coming due all at once in a series of climate events and wars that accelerate each other into a series of feedback loops into yet more crises.

Covid restrictions are ending here too

Our Cabinet will meet on Monday and is expected to let Aotearoa-NZ’s remaining Covid restrictions on mask use lapse by the end of the week as case numbers and intensive care occupancy rates head back to February levels.

Marc Daalder from Newsroom wrote a strong commentary piece on this prospect:

This would be a foolhardy move, when even the Government's own variant plan spells out an uncertain future of recurring pandemic waves which represent "a substantial increase in the overall burden of disease".

The fortunate situation we find ourselves in is unlikely to last forever. New variants could push baseline case numbers to levels where masks and other protections are still warranted, as happened after the first Omicron peak.

New variants and rapidly waning immunity will also fuel new waves, necessitating the imposition of more stringent but short-lived health measures to flatten the curve and dampen transmission.

The problem is that, with no framework like the traffic lights or alert levels to enable the reintroduction of protections on either a semi-permanent or temporary basis, the Government simply won't. We'll all suffer a much higher burden of disease and death for that failure. Marc Daalder via Newsroom.

Have a great weekend.

Ka kite ano

PS: My apologies to subscribers and Peter who dialled into this week’s live ‘hoon’ webinar. I was a few minutes late due to a scooter battery issue. I would not do well in Mad Max world.

Share this post